Insurance protects your pressure washing business from costly accidents. Bonding protects your clients from dishonest or unfinished work. Here’s how they work together to help you win more jobs and build trust.

Pressure Washing Business Insurance vs Bonding: Who’s Protected and When

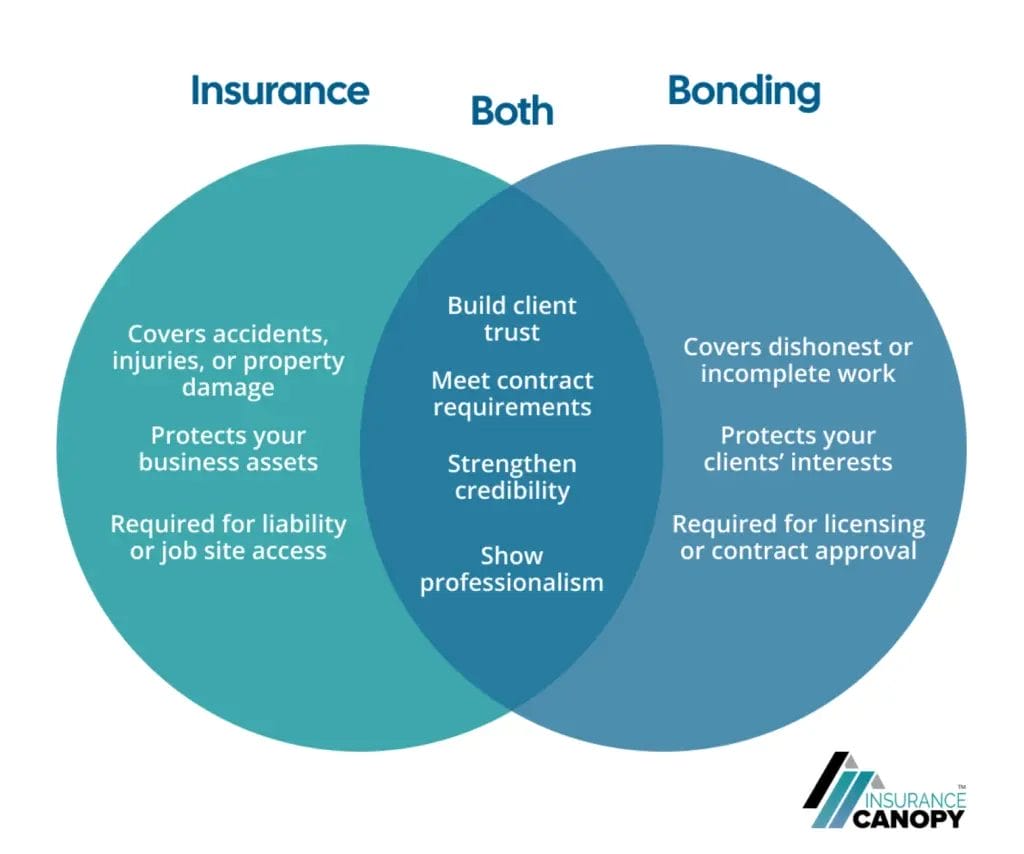

High-pressure jobs mean high risks and rewards. The right coverage makes sure those rewards become revenue for your business rather than an expensive claim. Pressure washing business insurance and bonds, like janitorial bonds, protect your business in different ways.

Pressure Washer Insurance vs Bonding: Quick Comparison

| Category | Insurance | Bonding |

|---|---|---|

|

Purpose |

Covers accidents and helps pay for property damage or injuries to others

|

Shows you’ll follow the rules of a contract, protecting the client from unfinished work or employee theft

|

|

Who it protects |

You and your customers

|

Your customer/client (not you)

|

|

Who pays for claims |

The insurer pays for covered claims up to your policy limit, after deductibles have been met

|

The surety company pays your client, then your business must repay the surety company

|

|

What proof you need |

Bond certificate/form, including a bond number and Power of Attorney (often listed in the license or bid paperwork)

|

|

|

Common triggers |

Third-party property damage, bodily injury, or certain advertising issues like libel or slander

|

You didn’t meet contract requirements, or your employee is accused of theft

|

|

Real examples |

Overspray on a car, a cracked window, or a water leak into a room

|

The HOA or agency requires a $10,000 license bond, or a client requests a janitorial bond

|

|

Cost factors |

Your revenue, crew size, type of work (residential/commercial), past claims, and coverage limits |

Bond amount, your credit/financials, bond type, and past claims |

|

Best for |

Protecting you and your customer when accidents happen — on the job and after work is done |

Meeting license and bid rules so you can win the job |

“””Policies, bonds, and related regulations vary by state and carrier. Contact us to talk with our non-commissioned, licensed insurance agents for more information.

Pressure Washing Risks: When You Need Insurance vs a Bond

Knowing when to use insurance or a bond is like choosing the right nozzle for your pressure washer — each one has its job, and skipping the right coverage can leave a mess behind. Here’s a quick look at which situations call for insurance and which need a bond:

Insurance

- Surface damage, broken windows, or chemical overspray → General Liability

- Equipment theft or damage while in transit → Tools & Equipment (Inland Marine)

- Business vehicle or trailer collision → Commercial Auto

- Employee injury or illness → Workers Compensation

Real Life Example

Manuel does pressure washing for local businesses. After he accidentally cracks a café window while cleaning the storefront, his general liability insurance covers the damage — saving him from an expensive mistake.

Bonds

- Employee steals from a client → Fidelity Bond

- Failure to complete a contract → Surety Bond (Performance Bond)

Real Life Example

Linda’s crew wraps up a poolside pressure washing job for a local homeowner’s association (HOA) when a nearby resident reports a stolen watch they’d left on a patio table. Her janitorial bond covers the loss, and Linda later repays the bond company for the claim.

Pro tip: If you’re new to the pressure washing industry and aren’t sure what all this “bonded and insured” talk means, head over to our Pressure Washing Insurance Guide for the complete overview.

Insurance vs Bonding: Which Is Better & Do You Need Both?

Neither a bond nor insurance is better than the other. They protect different sides of your business, and you might need both to meet contract requirements.

Insurance shields you from financial losses, while bonds protect your clients from dishonest or unfinished work. Most pressure washing businesses need insurance and bonding to stay protected and competitive.

Some cities and states won’t issue your pressure washing license without proof of insurance — and a bond might be required, too. Commercial clients, HOAs, and general contractors often expect both. If you’re unsure how to become licensed and bonded for pressure washing, start by reviewing your local and state requirements.

💦 Don’t Blast Your Budget 💸

You wouldn’t use the same nozzle for every surface — so don’t settle for one-size-fits-all insurance. Explore our comparison guide to find the best insurance for your pressure washing business.

How to Get Your Pressure Washing Business Bonded

Online surety bond companies and insurance agencies often sell bonds to small businesses. With Insurance Canopy, you can get bonded and insured all at once, plus browse instant-issue bonds through our online bond portal and get approved in minutes.

The U.S. Small Business Administration (SBA) also backs certain surety bonds through its guarantee program, which can help new or smaller pressure washing businesses qualify. Learn more about SBA-backed bonds on the SBA website.

Get Pressure Washing Business Insurance and Bonding Today

At Insurance Canopy, we want getting bonded and insured to feel like rinsing off the last layer of grime after a big job — you can finally step back, see your work shine, and know your business is protected.

Get a quote today for easy, affordable coverage that’s built for pros like you. And when you need support or have questions, our licensed insurance agents are ready to help in English and Spanish.

Common Questions About Pressure Washing Insurance vs Bonds

How Much is Pressure Washing Liability Insurance?

Liability insurance for pressure washers starts as low as $39 a month with Insurance Canopy, which is less than the national average. You can also choose the annual billing option and save up to 12% off your entire policy. Click here to learn more about the cost of pressure washing insurance.

What Types of Insurance Do Pressure Washers Usually Carry?

Most pressure washers carry a mix of liability and property coverage to protect their business, clients, and equipment.

The right cleaning business insurance for pressure washing depends on your services, job risks, and crew size — but typically includes general liability, tools and equipment coverage, workers compensation, and commercial auto insurance.

Remember: Not every insurance policy is the same. Always read your insuring agreement, conditions, and exclusions to know what parts of your business and services are covered.

How Fast Can I Get Insured or Bonded?

With Insurance Canopy, you can get insured and bonded in just a few minutes. Simply get a quote through our online portal, answer a few questions about your business, then add the coverages you need.

Once you’re done purchasing insurance, we’ll direct you to our bond portal, where you can find and purchase the bond you need.

What Proof Do Clients Want: ACORD/COI or a Bond?

For insurance, clients want to see a Certificate of Insurance (COI), sometimes called an ACORD form. Often, you’ll need to add them as an additional insured. They might also request a waiver of subrogation, all things you can do when buying a policy.

For bonds, most clients need to see a bond form and/or number, which is usually listed at the top of the bond form. You can view examples of bond forms in our bond portal.

Does a Bond Cover Damage I Cause on the Job?

No. Bonds protect the client if you fail to meet a contractual requirement, such as an unfinished job or employee misconduct. Damage that you cause is typically covered under a general liability insurance claim.

Kyle Jude | Program Manager

Kyle Jude is the Program Manager for Insurance Canopy. As a dedicated program manager with 10+ years of experience in the insurance industry, Kyle offers insight into different coverages for small business owners who are looking to navigate business liability insurance.

Kyle Jude is the Program Manager for Insurance Canopy. As a dedicated program manager with 10+ years of experience in the insurance industry, Kyle offers insight into different coverages for small business owners who are looking to navigate business liability insurance.