“It’s time to hire some help.”

As your small business grows, take pride in the milestones! It’s validation that betting on your idea was the right choice. But once you bring on others to work with you, you take on new responsibilities and risks, which means your insurance needs change, too.

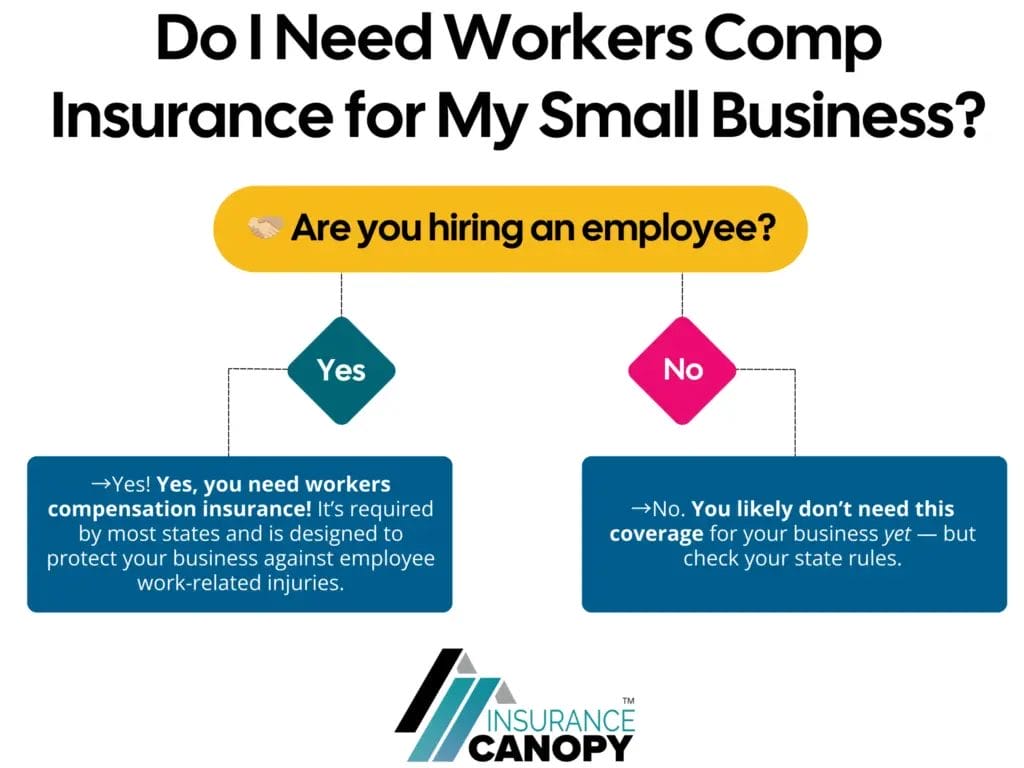

Let’s start with the most essential, and often legally required, protection you must add: workers compensation insurance.

Insurance for Hiring Your First Employees

Key Takeaway: You’re typically required to carry workers compensation insurance coverage if you have one or more employees, but the rules vary by state.

Why Hiring Changes Your Small Business Insurance Needs

As a solopreneur, your focus is on safeguarding your business of one against liability claims. Once you hire even a single employee, you take on the additional responsibility of protecting your team and complying with state laws.

Before hiring, your small business insurance is likely sufficient with general and professional liability coverage, plus a few add-ons for your business gear or vehicle. Now, with employee-related risks in this mix, you need to level up your insurance policy.

Even though you’re in the first stages of expanding, you’re entering a field where millions of work accidents happen every year — 2.6 million injuries in private industry in 2023 alone.

The bottom line is that accidents happen, and if you’re hiring, you need to be able to take care of employees if things go wrong while they work. Carrying workers comp coverage is precisely how you do that!

Understanding Workers Compensation Coverage for Small Businesses

Workers compensation insurance is coverage for your employees if they get injured or become ill while working for your business.

It doesn’t matter whose fault the injury is: workers comp is designed to kick in and pay for your employee to receive the treatment they need to get better and back to work. In fact, it’s called a “no-fault” policy because employees don’t have to prove negligence to receive benefits.

This coverage differs from your general liability policy, which protects your business if it accidentally causes harm to others (clients or customers), in that it helps you take care of your own: employees who work for you.

Here’s how workers compensation works.

If your employees…

- Get injured on the job

- Become ill because of their work

- Are hurt while performing work duties off-site

- Experience mental or emotional stress from a work incident

- Suffer from repetitive motion injuries from work

Then workers compensation could cover…

- Medical bills

- Lost wages

- Rehabilitation costs

- Death benefits

- Potential lawsuit expenses

Its purpose is two-fold: 1) protecting your employees if they get hurt, and 2) safeguarding your business, financially, so you don’t have to pay out of pocket to make things right.

Ultimately, workers compensation gives you peace of mind to focus on your growing business — and all the amazing possibilities ahead.

Pro Tip: New to business insurance and need to back up? Check out our explainer on the types of coverage small businesses need.

When Is Workers Comp Required for Small Businesses?

Workers comp laws for small business owners vary by state, but the most important thing to know is that 48 states (Texas and South Dakota excluded) require you to carry it. It’s just a matter of when it becomes a legal requirement for your business.

The specific rules are typically based on the number of employees you hire. Some states mandate coverage with your very first hire, and some allow more flexibility.

Examples of Workers Compensation Rules by State

| State | When Coverage Becomes Mandatory |

|---|---|

|

1 or more employees |

|

|

1 or more employees |

|

|

4 or more employees (1+ for construction) |

|

|

5 or more employees |

|

|

Not required; highly recommended |

Depending on where your business operates, there may be exceptions for:

- Interns

- Volunteers

- Family members

- Independent contractors

- Employees based in other states

Make sure you understand the employment status of those you bring on to work with you. And always check your state’s official Department of Labor website for the most current workers laws before you hire your first employee.

➡️ If you don’t carry the proper insurance, you face potential fines for violating your state’s workers compensation laws

➡️ Even if your state doesn’t require you to carry workers compensation insurance, it’s essential for protecting your business in case employees get hurt on the job

Pro Tip: Are you expanding your business in other ways, like selling retail products or significantly increasing revenue? Explore essential insurance for growing businesses.

How to Add Workers Comp Coverage to Your Policy

Getting a free workers compensation insurance quote from Insurance Canopy is simple — easier than combing through hundreds of job applicants! Simply fill out our online application with details about your business. Your quote will arrive right in your email inbox.

Some information you’ll need:

- Your business’ legal status

- Your federal employer ID number

- Your estimated annual payroll

- The number of employees on your payroll

- Details on owners, partners, or relatives to include/exclude

Insurance Canopy Grows With Your Business

Growing your small business is a big deal. Insurance Canopy’s here to support you every step of the way with affordable, top-rated insurance that doesn’t get in the way of your day-to-day!

Have questions about workers compensation coverage? Our licensed, U.S.-based support agents have answers and can help you get the exact coverage you need. Call us 844.520.6993 to speak with a real person.

Whether you’re hiring one assistant or an entire team, Insurance Canopy’s coverage is tailored to you. Expand your business confidently, knowing you’re compliant and protected against costly “what if” moments.

FAQs About Workers Comp for Small Businesses

Do Small Business Owners Need Workers Comp for Their First Employee?

Small business owners need workers comp insurance for their first employee and beyond. This essential coverage helps pay for work-related injuries and illnesses and is legally required in most states.

What Happens if I Don’t Have Workers Comp?

If you don’t have workers compensation, you may need to pay state penalty fees and cover your employees’ medical bills (plus any legal fees) on your own.

How Much Does Workers Comp Cost for Small Businesses?

On average, Insurance Canopy policyholders pay $105/month for workers comp coverage. Your premium costs vary depending on factors such as your industry, the number of employees you have, and the type of work your employees perform.

Does Workers Comp Cover Independent Contractors?

Typically, workers compensation insurance doesn’t cover independent contractors, as it’s designed for W-2 employees. State requirements vary, so it’s crucial to verify contractor coverage rules and speak with your insurer to make sure you’re compliant and protected.

Kyle Jude | Program Manager

Kyle Jude is the Program Manager for Insurance Canopy. As a dedicated program manager with 10+ years of experience in the insurance industry, Kyle offers insight into different coverages for small business owners who are looking to navigate business liability insurance.

Kyle Jude is the Program Manager for Insurance Canopy. As a dedicated program manager with 10+ years of experience in the insurance industry, Kyle offers insight into different coverages for small business owners who are looking to navigate business liability insurance.