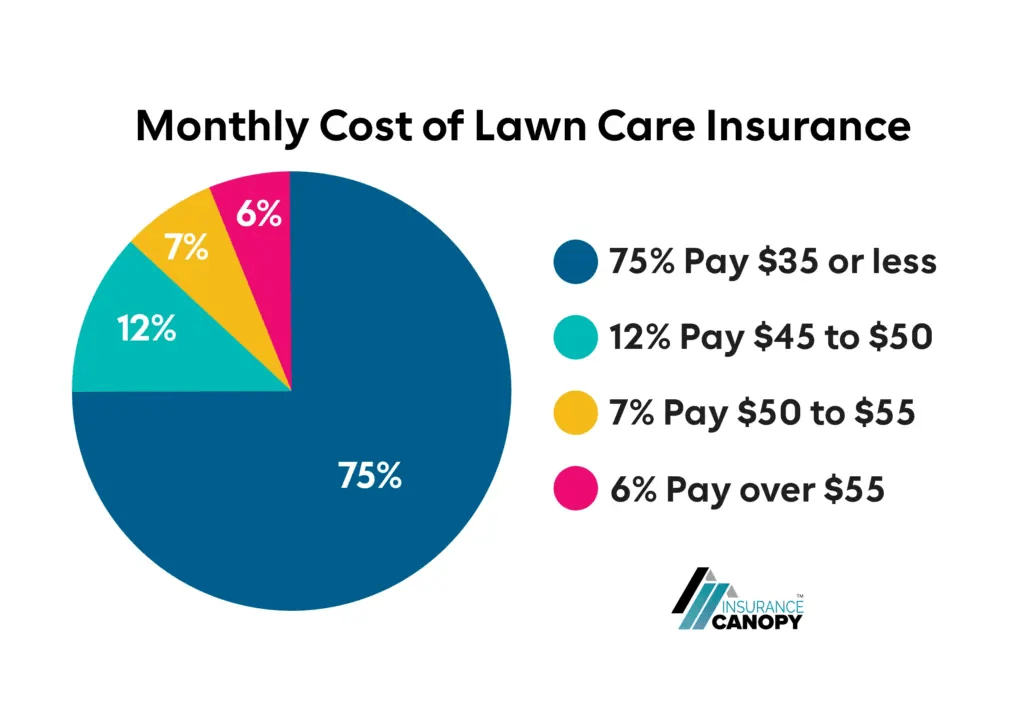

Lawn Care Insurance Cost

While you can’t prepare for every accident, you can protect your business from the costs that come with one. Having the right insurance protects your work, equipment, and income when things go sideways. Lawn care insurance is a small investment in your peace of mind and the financial stability of your business.

How Much Does Lawn Care Insurance Cost?

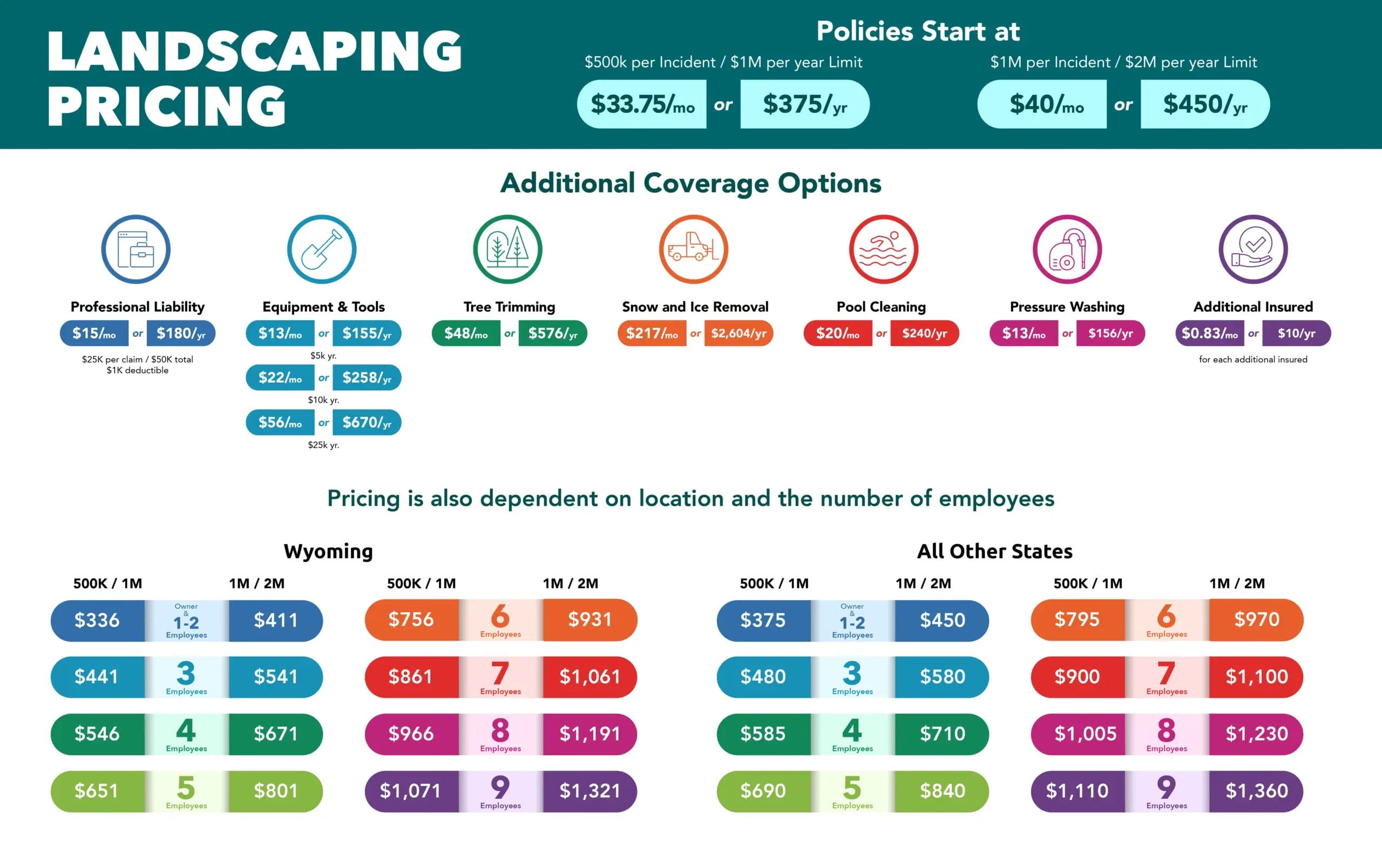

Insurance Canopy’s lawn care insurance starts at only $33.75 per month or $375 per year for base coverage.

This starting price works for many solo operators and small crews, but your final premium depends on things like the number of employees you have, the coverage limits you choose, and whether you add options like tools and equipment, professional liability, or commercial auto.

What Types of Payment Plans Are Available?

Insurance Canopy offers affordable monthly and annual payment options for your lawn care insurance.

Monthly payments lower your upfront cost and spread payments across the year. This makes it easier for lawn care businesses to manage cash flow changes throughout each season. Monthly billing includes a $2 fee.

Annual payments save you money over time. No monthly fees mean a lower total cost over the life of the policy. If you’re looking for year-round coverage at the lowest price, annual billing might be a better option.

How Much Does Each Type of Coverage Cost?

General Liability Insurance: $31 a Month or $336 a Year

General liability coverage protects your lawn care business from expensive claims involving third-party bodily injury and property damage. It can also pay legal defense costs and medical expenses for those covered accidents.

Tools and Equipment: $13 a Month or $155 a Year

Tools and equipment insurance, also called inland marine, helps pay for repairs or replacements if your gear is damaged or stolen in transit, at a job site, or while in storage. This includes detached trailers, mowers, and other common lawn care equipment.

Cyber Liability: $8.25 a Month or $99 a Year

Cyber liability protects your business if sensitive client information or payment data is exposed during a cyber attack. This includes ransomware, data loss, and security breaches. It can cover expenses such as legal fees, credit monitoring, notification costs, and more.

Professional Liability: $15 a Month or $180 a Year

Professional liability protects your business when a client claims your work, advice, or professional service caused a financial loss. It steps in to pay the cost of defending a claim and resolving it, up to your policy limit.

Tree Trimming: $48 a Month or $576 a Year

Tree trimming coverage extends your coverage to protect you from the hazards of tree work. It covers liability for pruning, shaping, and routine trimming where falling limbs, property damage, or bodily injury are more likely.

Snow & Ice Removal: $217 a Month or $2,604 a Year

Snow and ice removal protects your business from winter exposures — slip-and-fall claims, property damage from plowing or de-icing, and related liability from clearing driveways, walkways, and small residential or multi-family areas.

Pool Cleaning: $20 a Month or $240 a Year

Pool cleaning insurance covers risks associated with servicing pools, including accidental damage to pool finishes or equipment, injuries related to pool work, and liability arising from chemical handling or service-related incidents.

Pressure Washing: $13 a Month or $156 a Year

Pressure washing coverage protects against exposures from high-pressure cleaning, such as surface damage, overspray onto nearby property, water intrusion, and related liability or defense costs.

Additional Insured: $0.83 a Month or $10 a Year

Additional Insured coverage adds a client or general contractor to your policy as a covered party if a contract requires it. This protects them from covered losses under your policy and helps you meet proof-of-insurance requirements.

Workers Compensation

Workers compensation protects your crew and payroll if an employee suffers a work-related injury or illness. It helps pay for an employee’s medical expenses, rehabilitation, and even a portion of their lost wages.

Business Service Bond

Business service bonds build client trust by offering financial protection if one of your employees steals property or money from them. It gives customers peace of mind and reimburses them for the covered loss.

Commercial Auto

Commercial auto insurance protects your company-owned vehicles if they’re vandalized, stolen, or involved in an accident. It also covers repairs to your vehicles and medical bills for injuries due to an accident.

Still have questions regarding our policies? Feel free to reach out to our licensed insurance agents. We are available Monday through Friday from 8am–8pm ET.

What Factors Affect Lawn Care Liability Insurance Cost?

Crew Size

The more employees you have on payroll, the more exposure to lawn care risks you take on. A larger crew often means you pay a higher premium.

Optional Coverages

Add-ons like tools and equipment or professional liability expand your coverage, but also increase your premiums.

Claims History

Insurance companies usually charge higher premiums for businesses with a claims history, leading to an increase in your costs.

Lawn Care Liability Insurance Cost Factors

Here’s how your crew size affects the price of your lawn care insurance program:

How Can I Cut the Cost of Lawn Care Insurance?

An easy way to lower your lawn mowing business insurance costs is to choose annual billing over monthly payments.

You can also keep costs low by trying these risk management strategies to manage exposure to job-site risks:

- Give your mowers, trimmers, and blowers a once-over before you start working to prevent equipment failures and accidents.

- Keep your crew and customers safe by maintaining a safe worksite. Do regular safety checks for tripping hazards on walkways, and keep an eye out for other preventable accidents.

- Work within the scope of your policy and add-on coverages. This means avoiding tree work within 15 ft of power lines and not pressure washing above two stories.

Why Insurance Canopy for Lawn Care Insurance?

Need a no-nonsense lawn care insurance policy that meets you where you work? We’ve got you covered, rain or shine:

- Affordable Monthly or Annual Payments

- Coverage that Scales with Your Crew Size

- Manage Your Policy Online 24/7

- Instant Certificate of Insurance (COI)

Lawn Care Insurance Coverage Details

The most your policy will pay in a 12-month policy period for bodily injury and property damage claims that you become legally obligated to pay due to your business services.

$2,000,000

The maximum amount your policy will pay in a 12-month period for bodily injury and property damage claims that result from the products you use to perform your services. However, it does not cover products that are sold or distributed.

$1,000,000

The maximum your policy will pay for a bodily injury or property damage claim that you are legally obligated to pay due to your business services.

$1,000,000

The amount that your policy will pay for claims arising out of one or more of the following offenses:

- False arrest, detention, or imprisonment

- Malicious prosecution

- Wrongful eviction or wrongful entry

- Oral or written publications that slander or libel a person or organization

- Oral or written publication or material that violates a person’s right of privacy

- The use of another’s advertising idea in your advertisement

$500,000

Applies to damage by fire to premises rented to the insured and to damage regardless of cause to premises (including contents) occupied by the insured for 7 days or less.

$100,000

Optional Add-ons

Also known as “inland marine,” Equipment & Tools covers movable property such as mowers, edgers, and gardening supplies. This coverage pays to replace or repair your business gear if it’s stolen or damaged.

Note: This coverage excludes any structures or items permanently fixed to a single location.

$5,000/yr.

$10,000/yr.

$25,000/yr.

Also known as errors and omissions (E&O), Professional Liability coverage protects you from financial losses resulting from mistakes or negligence in your landscaping services. This includes advice or consultation you offer to a customer that causes bodily injury or financial loss.

$25K per claim up to $50K total

$1K deductible

$15/mo or $180/yr.

Liability coverage for landscaping businesses that perform residential snow removal services. This covers single-family homes, driveways, and small multi-family complexes.

Note: Services for commercial properties and public roads are not protected under Snow and Ice Removal coverage.

$217/mo. or $2,604/yr.

Covers landscaping businesses that provide pool cleaning, chemical treatments, and basic pump and filter repairs. Pool and Pond Maintenance protects you from expensive claims if you or an employee accidentally damages a client’s pool or equipment during service.

$20/mo. or $240/yr.

Protects landscaping businesses that service residential driveways, fences, patios, and exterior walls. However, the business must use non-toxic, water-based chemicals and clean surfaces less than two stories tall.

$13/mo. or $156/yr.

Some lawn care jobs require temporarily adding contractors or clients to your policy as additional insureds. Pricing starts at just $10 per year per insured. If you use independent contractors to assist with jobs, the coverage requires that you are listed as an additional insured on their policy.

$0.83/mo. or $10/yr. (each additional insured)

Provides financial compensation to employees who suffer work-related illnesses or injuries, including lost wages, medical expenses, and rehabilitation costs. It also covers your legal fees if an employee sues you over a workplace injury or illness.

Bonds protect your clients from financial loss if you are unable to complete a contract. They also ensure you meet all legal requirements necessary for jobs.

Protects your business from financial loss caused by phishing scams, ransomware, and other cyberattacks. If your company processes payments and stores client information digitally, cyber liability is essential for securing your business.

Lawn care professionals typically rely on a fleet of vehicles to transport landscaping equipment and crew members. If an employee gets into an accident on the way to a job site, commercial auto coverage can cover third-party injuries and damages. Additionally, it also covers vandalism and theft of your equipment.

How Do I Get a Quote?

Complete our quick online application and get your free quote in minutes. Just tell us a little about your business and what coverage options you need, and we’ll handle the rest. You’ve got lawns to cut and jobs to finish — let’s get you same-day coverage without losing half the workday.

FAQs About the Cost of Lawn Care Insurance

What Coverages Raise the Cost of Lawn Mowing Insurance?

Add-on coverages like tools and equipment, professional liability, and additional insureds all add essential protection to your policy, but they do increase your premium.

Does Lawn Care Insurance Cover Stolen Equipment?

Your base lawn care policy doesn’t cover stolen equipment, so you’ll need to add tools and equipment coverage to protect your gear from theft or damage. This optional coverage helps pay for stolen or damaged equipment, such as mowers, trimmers, and other business-essential gear.

Can I Add an Additional Insured to My Lawn Care Program?

Yes, you can add a contractor, client, or HOA as additional insured for just $0.83 a month or $10 a year. This can help you meet certain client requirements and open up more opportunities to bid on jobs.

Clint Hale | Copywriter

Ohio-based copywriter Clint Hale leverages his experience as a bourbon and stout enthusiast to distill insurance into clear, simple language. He also holds a B.A. in Communication Studies from Kent State University. Before working at Insurance Canopy, he was a Senior Copywriter at an SEO marketing agency. Fully trained in all things insurance, Clint writes to help business owners find a well-rounded policy to meet their needs.

Ohio-based copywriter Clint Hale leverages his experience as a bourbon and stout enthusiast to distill insurance into clear, simple language. He also holds a B.A. in Communication Studies from Kent State University. Before working at Insurance Canopy, he was a Senior Copywriter at an SEO marketing agency. Fully trained in all things insurance, Clint writes to help business owners find a well-rounded policy to meet their needs.