If alcohol is part of a wedding, the host typically needs liquor-related coverage; any bartender or alcohol vendor needs coverage for their role; and the venue will likely require proof in the form of a COI.

Let’s just say this upfront: When alcohol is involved, everyone likes to assume someone else has it covered…

The venue points to the bartender.

The bartender points to the host.

The host assumes it’s included somewhere already.

Then a contract mentions “liquor liability” and an “event insurance COI,” and suddenly it’s not so clear. Here’s the part that makes this easier: If alcohol is present, the host needs to carry liquor-related coverage. The only question is, what kind?

TL;DR: Liquor Insurance for Weddings

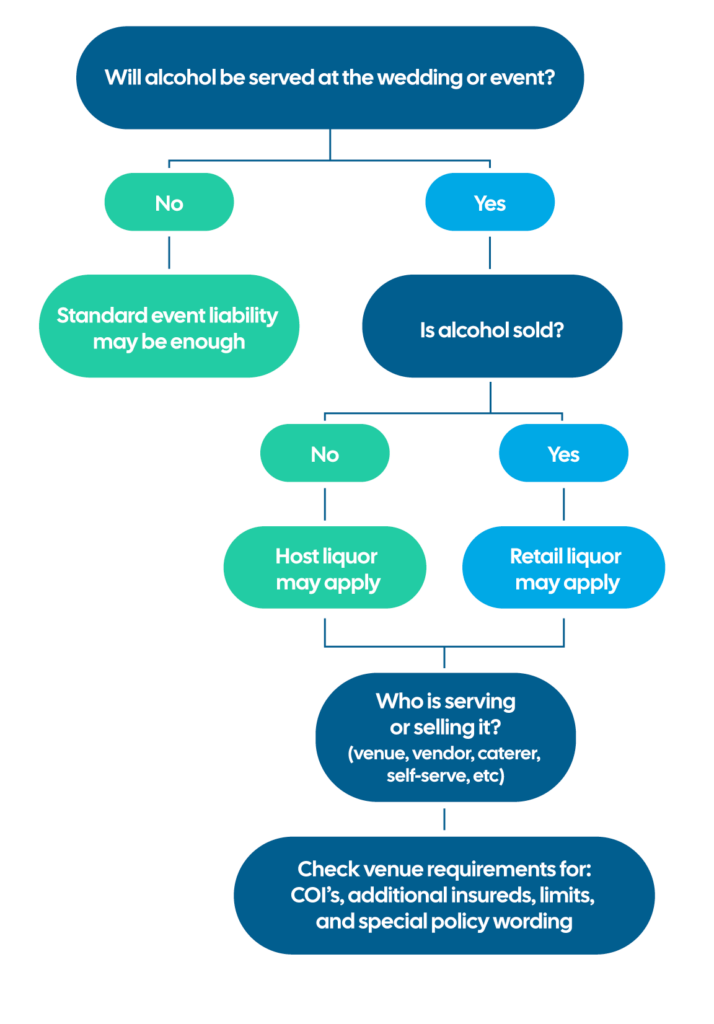

If alcohol is at your wedding, your event host insurance needs liquor coverage as well.

- If alcohol is served complimentary, you need host liquor coverage

- If alcohol is sold, you need retail liquor coverage

- If a vendor is serving or selling, they need liquor liability insurance

- Most venues will also ask for proof (a COI), so it’s worth sorting this out early

What Is Wedding Alcohol Liability?

At a wedding, “alcohol liability” means the party that could be held responsible if alcohol leads to injury, damage, or a claim.

That might look like:

- A guest being overserved and causing an accident

- Property damage tied to intoxication

- A third-party claim after someone leaves your event

Who Needs Liquor Insurance for a Wedding?

Before anything else, look at how alcohol is being handled at your wedding. That’s what drives responsibility, coverage, and what your venue will ask for.

| Alcohol Service | Who Needs Insurance | What Venues Tend to Ask for |

|---|---|---|

|

Venue provides bar + staff |

– Event host (host liquor insurance) |

– Event host COI |

|

Bartending company |

– Bartender (liquor liability insurance) – Event host (host liquor insurance) |

– Bartender COI |

|

Caterer serving alcohol |

– Caterer (liquor liability insurance) – Event host (host liquor insurance) |

– Caterer COI |

|

BYOB / self-serve |

– Event host (host liquor insurance) |

– Event host COI |

|

Cash bar / tickets |

– Bartender (liquor liability insurance) – Event host (retail liquor insurance) |

– Bartender COI |

You can often find alcohol insurance for your wedding offered with many wedding insurance policies. With Insurance Canopy, we automatically include host liquor coverage and offer retail liquor coverage as an optional add-on.

How Do I Know What Wedding Alcohol Insurance I Need?

If you’re staring at your venue contract or a vendor email right now, you probably just want to know you’re doing this right.

Start with these three questions:

| Question | If Yes... | What That Means |

|---|---|---|

|

Are you providing any of the alcohol? |

– You’re supplying alcohol in any way |

– You need host liquor liability coverage |

|

Is any alcohol being sold? |

– Cash bar |

– You need retail liquor liability |

|

Is someone serving alcohol? |

– Bartender |

– You need host liquor coverage |

If you’re thinking “okay… so multiple people might need a policy,” you’re right. Most weddings require both the host and the bartender to have insurance. For example:

- You hire a bartender for an open bar → You need host liquor coverage

- Your bartender serves it → The bartender needs liquor liability

- Your venue is listed on both your event host COI and the bartender’s COI

That’s normal, and it just means everyone is covered for their role.

Host Liquor vs Retail Liquor Liability for Weddings

This is one of the most common points of confusion, but it comes down to whether the alcohol offered to guests is free or sold.

- Host liquor liability: Applies when you’re providing alcohol at no cost to guests

- Retail liquor liability: Applies when alcohol is being sold in any way

For weddings, that usually looks like:

- Open bar or BYOB = Host liquor coverage

- Cash bar or drink tickets = Retail liquor coverage

- Alcohol services run by the venue = Host liquor coverage

If you’re not sure, a good rule of thumb is this: If guests are paying for alcohol, it’s often considered retail liquor. If it’s offered complimentary, it’s considered host liquor.

What Your Venue Is Asking For (COI + Additional Insured)

When your venue asks for a Certificate of Insurance (COI), they want proof that the right coverage is in place before alcohol is served.

Here’s what that actually means:

- Certificate of Insurance: A document that shows a policy exists

- Additional Insured: The venue is added to the policy for protection

- Certificate Holder: The venue (they’re receiving a copy of the document)

Most of the time, your venue wants to be an additional insured, but you may occasionally have one that just wants to be a certificate holder. There is a difference between the two, so just be sure to add them correctly based on their request.

When reviewing your COI, your venue will typically look for:

- The correct event date

- The full legal venue name (exactly as listed in your contract)

- The right type of coverage (host vs retail)

- Coverage limits that meet their requirements

If you’re working with vendors, they’ll usually need to send their COIs directly to the venue (and you’ll want a copy for your records, too).

What If My Venue Rejects My Wedding COI?

If your venue rejects your COI over the liquor insurance for your wedding, the first step is to breathe. You’re not rejected from the venue; you just need to re-evaluate your coverage and make adjustments.

The most common issues are small, but they matter:

- The policy date is incorrect or missing (coverage may not be for the event dates)

- The venue name doesn’t match the contract exactly

- The venue isn’t listed as additional insured

- The wrong type of coverage is shown

- Coverage limits don’t meet venue requirements

Quick Wedding Alcohol Insurance Checklist: Host vs Planner

If you just want to make sure everything’s handled, this is the fastest way to do it.

If You’re the Event Host:

- Confirm what your venue requires

- Confirm what your vendors carry

- Make sure you have the right coverage (host or retail)

- Collect COIs from vendors

- Check that your venue is listed as an additional insured

If You’re the Event Planner:

- Request COIs from all alcohol-related vendors early

- Confirm your coverage type matches your festivities

- Check dates, names, and additional insured wording

- Make sure coverage limits meet venue requirements

- Track everything in one place

Cheers to Choosing the Right Coverage

Alcohol insurance for weddings is one of those things that sounds more complicated than it actually is. Once you know how your alcohol is being handled, it gets a lot easier to figure out what coverage you need.

Get a quote for wedding event insurance today and check this off your list!

Are you a wedding planner?

Get event planner insurance

FAQs About Alcohol Liability Insurance for Weddings

Do I Need Wedding Alcohol Insurance If Alcohol Is Free?

Yes, you need wedding alcohol insurance if the alcohol is free. Complimentary alcohol service requires host liquor liability coverage, which is included with all Insurance Canopy event host policies.

Does the Venue’s Insurance Cover Me?

No, the venue’s insurance does not cover you for liquor liability. If the venue provides an in-house bartender, you’ll still need host liquor liability coverage (regardless of whether the alcohol is served or sold from the venue).

What If We’re Doing BYOB?

If you’re doing BYOB, you’ll still need host liquor insurance. Even without a licensed bartender or catering service, you’re responsible for alcohol-related accidents caused by the drinks provided at your event.

What’s the Difference Between Liquor Insurance for a Wedding and Event Liability?

The difference between liquor insurance for a wedding and event liability is:

- Event liability covers general incidents (like injuries or property damage)

- Liquor liability specifically covers alcohol-related incidents

Depending on your setup, you may need both.

What If My Bartender Won’t Provide a COI?

If your bartender won’t provide a COI, that’s a contract to reconsider. Most venues require proof of coverage before allowing alcohol service, and moving forward without it can leave gaps. You may need to look for alternative bartending options to meet your venue’s requirements.