A caterer’s server gets injured. A DJ scratches the dance floor. A COI expires the day before setup. Suddenly, everyone turns to the event planner asking, “Who’s covered?” or worse, “Who pays?”

A vendor event checklist lists the coverage and documentation vendors must provide before working at an event. As the event planner, it can be your job to make sure everyone’s proof of insurance is in order. Gathering and checking COIs from vendors you hire is no one’s favorite part of event planning, but it can seriously limit the chaos if something goes wrong.

When you know what proof to ask for, you can confidently get what you need every time (without being an insurance expert). In this guide, you’ll get these event planner resources:

- The vendor insurance venues usually expect

- What documentation event planners should collect from vendors they hire

- How to review a Certificate of Insurance (COI) quickly

- A simple event planner vendor checklist you can use again and again

Requirements vary, but once you know the basics, you can feel event-ready every time.

Vendor Insurance for Event Planners: What to Require From Every Vendor

Depending on whether you hired the vendors or the event host did, your role in requiring, gathering, and checking vendor COIs will be different. Let’s start with the basics.

Instead of reinventing the wheel for every event, it’s helpful to have a default set of basic insurance details you’ll collect from vendors that you hire. You’ll always follow the venue’s contract and requirements first, but your own checklist offers a consistent way to request and review what’s needed.

Let’s start with the venue’s typical requirements.

Venues’ Most Common Insurance Requirements

The language of vendor insurance can sound more intense than it really is. Rules vary by venue, but most have similar baseline requests for protecting themselves. Once you’ve seen them a few times, they’ll start to look familiar.

New to insurance? We offer a detailed breakdown in our vendor insurance requirements guide.

Here’s what to expect:

- A Certificate of Insurance (COI): Also called proof of insurance, this is a one-page snapshot of a vendor’s insurance, kind of like a receipt. Here’s a quick guide on How to Read a COI.

- General Liability Insurance: This is the vendor’s main coverage, and it protects against accidental physical injuries and property damage to others. The typical limit venues require is $1M per occurrence coverage and a $2M aggregate limit.

- Additional Insured: This means the vendor’s policy could also provide protection for someone else if they get named in a claim because of the vendor. Venues may require themselves, the client, or even you as the planner to be listed as additional insureds on the policy and the COI.

- Waiver of Subrogation: This is special wording that prevents the vendor’s insurance carrier from trying to reimburse costs from the venue after paying a claim.

- Primary and Noncontributory: This means the vendor’s policy will respond first before other insurance policies that cover the same things. Venues usually require it so that the vendor’s policy is used up first before their own policy kicks in after an accident.

Basic Vendor Coverage to Request

For most events you plan, every vendor you hire should be able to provide:

| Requirement | Description |

|---|---|

|

General Liability Insurance |

The vendor’s main liability coverage |

|

Current Certificate of Insurance (COI) |

Must show coverage type, limits, policy dates, and insurance carrier |

|

Additional Insured Status (if needed) |

Must list the venue, the client, and, when required, you as Additional Insureds |

And that’s it! None of those requirements is anything unusual, so most professional vendors will have provided them before. If the venue asks for extra requirements, add those to your list.

At a Glance: What to Require for Specific Vendor Types

Along with those basics, some venues also require higher-than-usual limits or extra coverage for certain vendors. This is usually because their service or the way they run their business introduces more or different kinds of risk.

Here are common types of vendors you might be working with, plus extra requirements and potential red flags to watch for:

| Requirement | Description | Good to Know |

|---|---|---|

|

Caterer / Food Service / Bar Service / Bartenders |

Liquor Liability (if providing or serving alcohol) Workers Comp (if they have employees) Commercial Auto (if they provide delivery services) Additional Insured status for venue, client, and/or planner |

Most common miss: no liquor coverage Confirm policy dates include setup and teardown |

|

Rental Company (tables, chairs, tents, and linens) |

Commercial Auto (if they provide delivery) Additional Insured status for venue, client, and/or planner Umbrella/Excess if tents or staging are involved |

Tents and staging usually trigger stricter venue requirements |

|

DJ / Band / Entertainers |

Additional Insured (venue or client) |

Red flag: “I’ve never needed this before.” Additional Insured is not an unusual request. |

|

Photographer / Videographer |

Professional Liability (E&O) for deliverables or heavy contracts Additional Insured status for venue, client, and/or planner |

Verify limits if the venue is strict |

|

Florist or Decorator (including installation) |

Additional Insured status for venue, client, and/or planner |

If hanging or attaching décor, treat as higher risk |

|

Transportation (shuttle, limo, party bus, delivery vehicle) |

Additional Insured status for venue, client, and/or planner Commercial auto (higher limits for passenger transport) |

Personal auto ≠ commercial auto. Confirm passenger coverage. |

Caterer / Food Service / Bar Service / Bartenders

Common Requirements

- Liquor Liability (if providing or serving alcohol)

- Workers Comp (if they have employees)

- Commercial Auto (if they provide delivery services)

- Additional Insured status for venue, client, and/or planner

Good to Know

- Most common miss: no liquor coverage

- Confirm policy dates include setup and teardown

Rental Company

Common Requirements

- Commercial Auto (if they provide delivery)

- Additional Insured status for venue, client, and/or planner

- Umbrella/Excess if tents or staging are involved

Good to Know

Tents and staging usually trigger stricter venue requirements

DJ / Band / Entertainers

Common Requirements

Additional Insured (venue or client)

Good to Know

Red flag: “I’ve never needed this before.” Additional Insured is not an unusual request.

Photographer / Videographer

Common Requirements

- Professional Liability (E&O) for deliverables or heavy contracts

- Additional Insured status for venue, client, and/or planner

Good to Know

Verify limits if the venue is strict

Florist / Decorator

Common Requirements

- Additional Insured status for venue, client, and/or planner

- Equipment Insurance

Good to Know

If hanging, installing, or attaching décor, treat as higher risk

Transportation

Common Requirements

- Commercial Auto (higher limits for passenger transport, like shuttles, limos, and party buses)

- Additional Insured status for venue, client, and/or planner

Good to Know

Personal auto ≠ commercial auto. Confirm passenger coverage.

If the Event Host Hires Vendors Directly, Should I Still Check Their COIs?

This trips up a lot of event planners, because it’s a nuance that can make a big difference when it comes to liability.

Here’s the safest way to avoid taking on extra risks when you don’t need to: the person or company who hires the vendors should be the one responsible for collecting and reviewing their insurance.

If you hire and manage vendors: always check that they have current and valid insurance by requesting a COI.

It’s on you to ensure that any vendors you hire, like caterers or DJs, have the required insurance by collecting and checking their COIs before hiring them. This is when you should use your event planner vendor checklist (download your copy below) to make sure everything looks correct.

If the event host hires vendors directly: always suggest that the event host collect COIs from vendors.

You may be tempted (or even asked) to manage and review vendors’ COIs, but this can be risky for you legally. When requirements come from a venue, host, or city, you’re not responsible for confirming that a vendor’s policy meets those requirements. Your role is to help communicate expectations, not to enforce or approve them.

Imagine this: you tell a wedding bartender hired by the couple that their insurance looks fine, only to find out later that they didn’t have the right liquor liability coverage. Now there’s a claim in jeopardy, and everyone’s blaming you.

Here’s how you can safely help with insurance needs if someone else hires the vendors, without reviewing or collecting COIs:

- Be aware of any host, venue, or city insurance requirements for events

- Help inform hosts and vendors about what’s expected from them

- Direct vendors and hosts to the venue, host, or city with the insurance requirement to verify their COI or ask follow-up insurance questions

Free Event Planner Vendor Checklist: Exactly What to Request

Time to put it all together. Here’s your reusable vendor checklist for event planners, including what to collect from vendors and how to track it in one place.

Systems and consistency matter in event planning, and this is an easy way to:

- Stay organized across multiple events

- Request the right documents from vendors

- Simply verification for limits, dates, and endorsements

- Help vendors respond faster to requests

- Show venues you’re a prepared professional

Track all the steps in one place and streamline event to-dos with your free checklist.

Help Vendors Meet Event Insurance Requirements with Insurance Canopy

Sometimes a vendor wants to work your event but doesn’t have the right coverage yet. That’s where event-friendly insurance can help.

Insurance Canopy offers simple, flexible liability coverage designed to meet common venue requirements. Vendors can apply online in minutes, choose a policy tailored to their business, get an instant COI, and add additional insureds or endorsements 24/7 through their online dashboard.

If a vendor needs help meeting your event’s insurance requirements, you can send them to Vendor Insurance Coverage from Insurance Canopy to explore affordable options.

Make It a System: Event Planner Resources to Manage Your Workflow

The easiest way to manage vendor COIs is to make checks part of your normal event management process. Once you build a system, collecting and reviewing them becomes just another box to check, like confirming final headcounts.

Here’s what the event management process for vendor insurance can look like in practice:

- Include insurance language in vendor agreements. A short clause in your vendor contracts can require vendors to maintain proper insurance and provide a COI when requested. That way, expectations are clear from the start.

- Request COIs when vendors are booked. As soon as a vendor is confirmed, send your COI request along with the contract or onboarding details.

- Set a clear deadline. Give vendors a due date for submitting their COI. Many planners aim for around two to four weeks before the event, so there’s time to fix anything that doesn’t meet requirements.

- Track everything in one place. Keep vendor insurance paperwork and your requirements checklist together with the rest of your planning documents.

- Do a quick check before event week. Before setup starts, confirm that higher-risk vendors (like caterers, bartenders, rental companies, or transportation providers) have submitted the required documentation.

Your system is organized, and you’re ready to go. Next on your list, getting vendors on board.

Communicating with Vendors: Easy COI Request Email Template

When you book a vendor, it’s best practice to send a COI request right away. Asking for proof of insurance can feel intimidating, but it doesn’t have to be complicated.

A simple message like this one can help vendors understand what they need with time to ask questions, strengthening those business relationships.

Subject: Insurance Certificate Request for [Event Name]

Hi [Vendor Name],

As part of [venue’s or your company’s] standard planning process, we collect proof of insurance from all vendors working the event.

Please send a current Certificate of Insurance (COI) showing:

- General Liability coverage

- Limits of at least [insert venue requirement]

- Policy dates covering setup, event day, and teardown

- [Venue, client, and/or planner name, if required] listed as Additional Insured

You can send the COI directly to me by [due date].

If your insurance agent needs the venue’s exact wording or event details, I’m happy to share that as well.

Thanks so much. This helps us keep everything venue-ready and running smoothly.

[Email signature]

Just copy/paste this template into your email and fill in the blanks to fit your event.

The 5-Minute Vendor COI Check for Event Planners

“But how do I verify that their COI is correct when I get it? I’m not an insurance expert.”

At this point, you might still be feeling nervous about handling proof of insurance. Once you get it, how do you know it has everything they need? Most of the time, you’re just confirming a few key details.

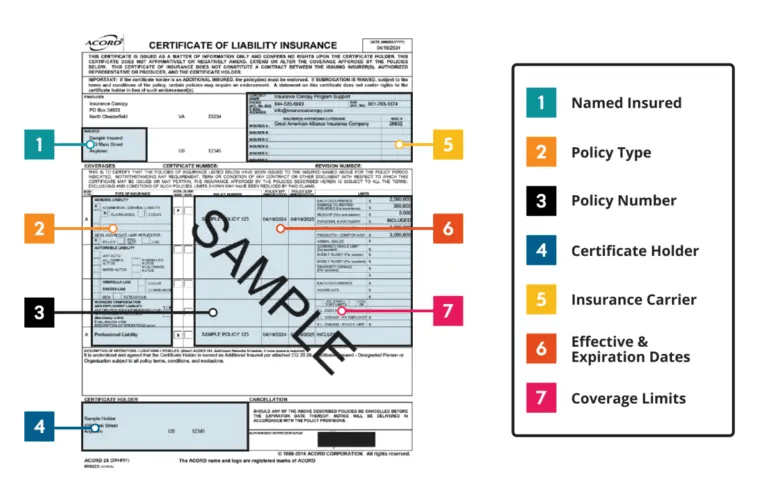

If you’re responsible for hiring the vendor (and verifying their insurance), here’s a quick way to review a COI. We’ll use this Labeled Example COI as a roadmap. (And don’t worry, we put these verification steps on your Insurance Requirements Checklist, too).

Here’s what to double-check and where to find it:

[ ] Confirm that the business names match

The vendor’s legal business name should match the name on their contract. If the venue or client needs to be listed on the COI, check that those names are spelled correctly, too.

Where to look: You can find the vendor name in the Named Insured section and the venue or client under Certificate Holder.

[ ] Check the policy type

Verify that the type of insurance your venue requires is what’s listed on the COI. This is usually just General Liability, but you may also need to look for Workers Compensation, Commercial Auto, Liquor Liability, or any others the venue requested.

Where to look: You can find the vendor’s insurance coverages in the Policy Type section of the COI. (It might also be called Coverages or Type of Insurance on the form.)

[ ] Make sure the limits meet the requirements

If the venue requires $1M per occurrence and $2M aggregate in General Liability, confirm those numbers appear next to the correct coverage.

Where to look: Find the coverage in the Policy type section, then follow the chart across to the Coverage Limits section to check for the right numbers.

[ ] Verify the policy dates

Coverage should include the entire event window. That means setup, event day, and teardown. For example, if a florist installs decor on Friday, but their policy starts Saturday, that’s a coverage gap they need to fix.

Where to look: Policy dates are listed in the Effective and Expiration Dates section next to the coverage where they apply.

[ ] Look for a checked Additional Insured box, if required

If the venue requires it, confirm that the venue, client, and/or you as the planner are listed as an Additional Insured.

Where to look: If an Additional Insured is added, you should see an Additional Insured checkbox filled in next to the Policy Type where it applies on the chart. In our example, the checkbox is labeled “Addl Insr.”

[ ] Confirm that the endorsements page is attached, if required

The venue might also require that the COI has an endorsements page attached to confirm their Additional Insured status, or other requested endorsements.

Where to look: The endorsements page will look something like the second page of this Example COI. Under “Schedule,” you can see “Name of Additional Insured Person(s) or Organization(s).” That’s where the venue’s, client’s, and/or your name should appear if everything is correct.

Common Vendor COI Issues Event Planners Should Watch For

- Expired policy dates

- Coverage limits below the venue’s requirement

- The wrong business entity is listed (for example, the vendor listed their own name rather than the name of their business)

- Missing insurance carrier information

- “We’ll send the updated certificate later”

Pro tip: If you’re responsible for collecting COIs and something looks off, here are some ways to fix it:

- Ask the vendor for clarification

- Request a reissued COI from the vendor’s insurance agent

- Send the venue’s exact wording to the vendor’s insurance agent, so they can match it properly.

Getting a corrected certificate usually isn’t a big deal (insurers expect it), so don’t hesitate to make sure everything looks right.

What If a Vendor Can’t Meet Your Insurance Requirements?

Occasionally, a vendor may not have the coverage your venue requires. That doesn’t automatically mean the vendor can’t work the event. It just means you’ll need to decide how to handle the gap between what they have and what they need.

These are a few common ways event planners work with missing vendor insurance requirements:

Option 1: Ask the vendor to update their coverage

In many cases, the vendor’s insurance agent can adjust their policy, increase limits, or add required endorsements like Additional Insured. It will usually cost the vendor more to get more coverage, but if it’s in their budget, this is usually the easiest solution.

Option 2: Adjust the vendor's role

If a vendor doesn’t carry certain coverage and can’t get what they need before the event, it’s possible to keep the vendor on but scale back what they do to avoid riskier activities. For example, if a caterer doesn’t have liquor liability, alcohol service may need to be handled by a licensed and insured bartender instead.

Option 3: Replace the vendor

If the venue requirements can’t be met or the risk is too high, you may need to work with a different vendor who already carries the required coverage.

Option 4: Request a venue or client waiver

In rare cases, a venue or client may agree to waive (not require) a specific requirement. If this happens, make sure the decision is documented in writing so everyone understands the risk.

Pro tip: You’ll be tempted, but here’s what not to do if a vendor can’t meet requirements. Even when you’re trying to keep the event on track, these shortcuts can create bigger problems later:

- Don’t accept expired COIs. Expired = not covered.

- Don’t assume a vendor is covered without a COI. It’s not unreasonable or unusual to ask for written proof of insurance (not just a verbal promise that it exists).

If a vendor isn’t sure about their insurance requirements or how to make changes, ask them to connect with their insurance agent or company. Vendors often assume it’s harder to make changes than it actually is. Insurers expect to provide and update COIs, so they should have a system in place.

Why Event Planners Still Need Liability Coverage (Even If Everyone Else Has It)

Requiring insurance from vendors helps protect the venue, your client, and the event itself. But vendor insurance doesn’t automatically protect you.

If something goes wrong at an event, multiple parties (including the planner) can get pulled into the claim, even if the issue started with a vendor. That’s why smart planners carry their own liability coverage (and why many venues and corporate clients also require you to show your own COI).

Event planner insurance is your safety net. It helps protect your business from claims involving your role in planning or coordinating the event with two key coverages:

- General liability, which can help cover the physical injuries or property damage to others tied to your planning services

- Professional liability, which is designed to respond if someone claims that your error, negligence, or failure to deliver caused them to lose money

Factoring in the variables and getting things done are your superpowers. Insurance supports what you do best with professional protection that’s ready for anything.

Keep Learning

- Considering coverage? Best Event Planners Insurance Compared lays out the pros and cons of popular policies.

- Still not sure how event insurance works? What Is Event Insurance and Who Needs It? breaks down all the details.

- Is event planning just one of your consulting services? Consider Consultant Insurance to protect other ways you work.

FAQs: Checking Vendor Insurance for Event Planners

What is a Vendor Certificate of Insurance (COI)?

A vendor Certificate of Insurance (COI) is a document that proves a vendor has active insurance coverage and shows the policy coverages, limits, dates, and insurer. Event planners and venues request COIs to confirm vendors meet insurance requirements.

Do event planners need to be listed as an Additional Insured on Vendor COIs?

Sometimes. If a venue contract requires it, the venue, client, and/or the event planner may need to be listed as an Additional Insured on a vendor’s policy. Being listed as an Additional Insured allows the vendor’s insurance to respond if a claim arises because of the vendor’s work that also names you.

Why do venues require vendors to have insurance?

Venues require vendor insurance to protect their property and reduce their liability risk. If a vendor causes injuries or property damage, then the vendor’s insurance can pay first toward making it right. This protects the venue and the vendor from having to pay for an expensive claim out of pocket if there’s an accident.

Do event planners need insurance if vendors and venues have it?

Yes, event planners need their own liability insurance, even if vendors and venues have coverage. If something goes wrong at an event, multiple parties can be named in a claim. Others’ insurance doesn’t automatically protect you, so you need your own coverage designed for your unique risks.

When should I ask vendors to send me proof of insurance?

You should request proof of insurance when the vendor is booked or shortly after they sign a contract. Many planners set a deadline of two to four weeks before the event, so there’s time to correct any issues with coverage, limits, or endorsements before setup begins.

{kind=link}