“Get your own insurance policy!” – you, probably (after receiving a request to add someone as an additional insured).

If you’re confused about when to add an additional insured endorsement, don’t worry. It doesn’t mean your client or event organizer is trying to hijack your coverage. It’s a common business ask you’ll face as a small business owner and a smart way to keep everyone protected.

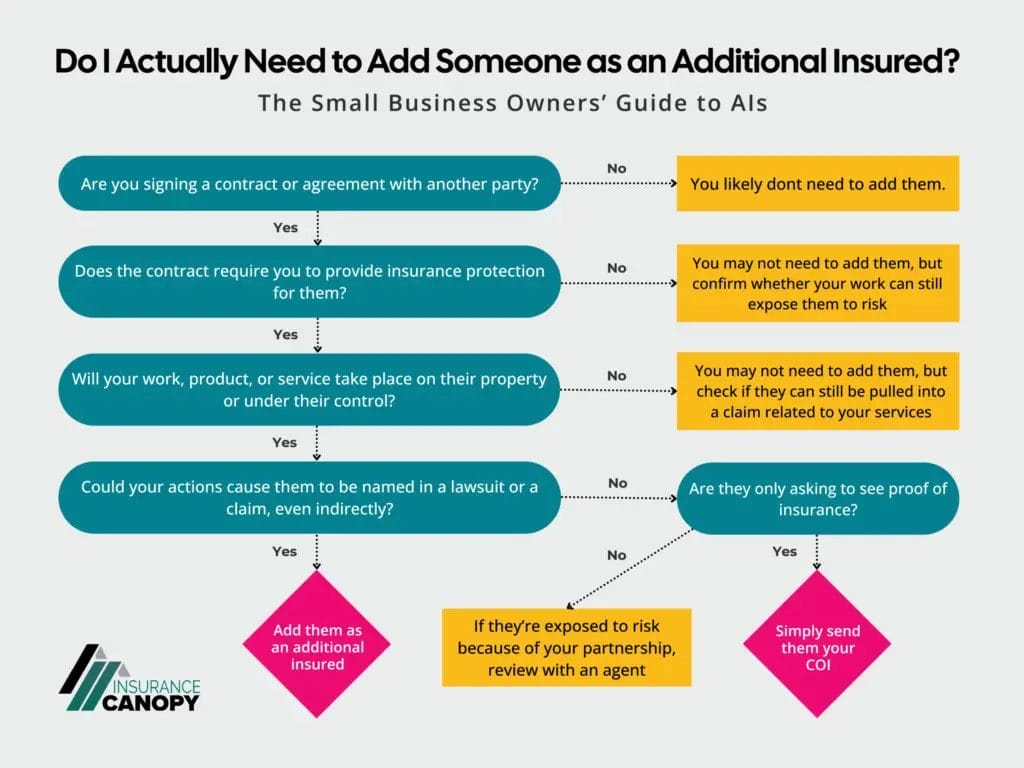

When Do I Need to Add an Additional Insured?

Common scenarios include:

✔️ If a client contract requires it

✔️ If you’re leasing property for your business

✔️ If you’re collabing with business partners

✔️ If a venue or event organizer requires it

✔️ If a city or county requires it

Quick Refresher

Additional Insured Meaning: An extension of your small business insurance coverage to another person or business who may be affected by your work. Think of it as a canopy protecting your business and your partners if you get caught in the same storm of claims.

Key Terms to Know When Adding Additional Insureds

Why would someone ask to be listed as an additional insured on your policy? Because it makes it less risky to work with you. They’re reassured that if something goes wrong, they’ll also be covered in case they get tangled up in the claim.

Here are some nuances about additional insureds and related terms to note.

Swipe for more →

| Term | What It Means | When It Applies |

|---|---|---|

|

Policyholder |

You, the small business owner with a policy in your name

|

When you purchase small business insurance

|

|

Additional Insured (AI)

|

Extended coverage for claims for a qualified third party

|

Business relationships like contract work, leases, or events

|

|

Someone who verifies your proof of coverage

|

Anytime another party needs to check that you have active insurance

|

|

|

Blanket AI

|

Automatic coverage for anyone you’re required to add by contract

|

Convenient for businesses with multiple contracts

|

|

Scheduled AI

|

Coverage listing specific names of parties you work with

|

Usually requested by clients, landlords, or events on your certificate of insurance (COI)

|

|

Primary & Noncontributory

|

Your policy pays first and won’t seek contributions from other active policies

|

Common in construction or government contracts

|

The most common request for small business owners is the scheduled additional insured, which means you’ll list the third party by name and send them a copy of your certificate of insurance as proof.

Common Scenarios That Call for Additional Insureds

Problem: A third party wants to be protected under your insurance in case they’re pulled into a lawsuit related to your work

Solution: No problem — just add them as an additional insured, provide a certificate of insurance to show they’re covered, and keep your contract rolling

Working Under a Client’s Contract

You’ve landed a new client, congratulations! Now put yourself in their shoes: Is there any chance your work might negatively affect them? If so, they’ll likely require you to list them as an additional insured before moving forward with the contract.

Clients ask to be added to your policy so their insurance won’t have to respond first if your business causes injury or property damage. This risk-transfer move helps everyone feel safer.

Client Contract Example: Massage Therapist

A corporate wellness program hires you to perform chair massages for employees during a wellness day. The company asks to be listed as an additional insured on your liability policy in case one of their employees claims they get injured. They want your insurance to defend them, too.

What Does Adding Additional Insureds Look Like?

- A third party requests to be listed as an AI on your policy

- You verify that it makes sense to extend your coverage to them

- You add them as an AI on your policy (it takes about five minutes online with Insurance Canopy)

- You send a copy of your COI with additional insured language to the third party

- Your next contract, lease, or event is a go!

Leasing Property for Your Business

Another common scenario you might encounter is adding a landlord as an additional insured. If you’re looking to rent space or equipment for your business, the property owner will want protection in case your operations cause third-party accidents.

It may seem trivial, but if one of your customers were injured at your business, they could potentially name your landlord in a lawsuit, simply because they own the property. An additional insured endorsement gives your landlord peace of mind against claims like these.

Property Lease Example: Fitness Professional

You find the perfect studio to take your Pilates business to the next level. Before you can move in, the landlord needs to be added to your policy as an AI. If a student slips and falls while attending your class, both you and your landlord can be covered by your insurance.

Pro Tip: When the lease ends, remove the property owner as an AI to prevent unnecessary exposure or clutter on your policy.

Collabing With a Business Partner

Say you’re teaming up with another company for a joint project, like a co-hosted event or a marketing collaboration. Your business partner may ask to be listed as an additional insured as a formality before jumping into the work.

When two businesses share clients or space, they face overlapping liability. If something goes wrong, a lawsuit could name everyone involved, even if one party wasn’t directly at fault.

Noticing a trend here? Like we mentioned earlier, additional insureds make it easier for other parties — whether clients, landlords, or partners — to say “yes” to working with you. Accidents (and “over-named” lawsuits) can happen to anyone.

Business Collab Example: Freelance Photographer

You partner with a wedding planner to provide bundled services for couples. Despite your longstanding relationship, they still ask to be added as an AI on your policy. If a guest trips over your lighting cord and sues both of you, the planner can be protected by your insurance, too.

Pro Tip: Whenever possible, use a reciprocal agreement where both parties add each other as additional insureds. Do not add a business partner whose risk profile is much higher than yours.

Meeting Venue or Event Requirements

A common scenario for adding additional insureds is to meet venue or event insurance requirements. It may seem like a hassle for something as short as a one-day event, but you likely won’t be able to participate as a vendor without it!

Event hosts and venues want protection in case your business operations harm attendees — even unintentionally. Think about the foot traffic and all the short-term interactions that can potentially lead to big claims.

Event Requirement Scenario: Food Truck Owner

Your mobile food business scored one of the best spots at the food truck festival. But your worst nightmare happens: a customer gets sick after eating your food and takes legal action against you and the organizer.

Because the event is listed as an additional insured, your policy can defend both of you from the liability claim. In this instance, the AI endorsement helps keep the event fun and safe for everyone.

Pro Tip: Most small business owners first realize they need insurance when applying for an in-person event! If you’re new to business ownership or just dreaming up a big idea, check out How to Start a Small Business: Step-by-Step Guide.

Working With Cities or Counties

Government entities have strict risk management policies, so if you secure a contract with a city, school district, or public agency, you will likely need to add them as additional insureds.

If your work causes damage or injury on public property, your insurance policy will kick in, rather than their tax-funded insurance programs. This helps ensure taxpayer dollars are protected and the financial responsibility falls on the private business performing the work.

Government Contract Example: Cleaning Company

Your small cleaning business lands a gig to clean a city building. It’s a big break for you, but one day, one of your employees forgets to leave a wet floor sign in a hallway. When a visitor slips and gets hurt, the AI endorsement on your policy helps cover both you and the city.

Key Takeaways for Adding AIs

- Always know why you’re adding someone to your policy

- Mutual risk should mean mutual coverage, so you’re both protected

- Keep documentation current (make sure AI details are correct and up to date)

- Review “primary and noncontributory” language to know whose policy responds first

- Ask your agent if you have questions about what is and isn’t covered by the AI endorsement

Learn how to add an additional insured to your Insurance Canopy policy. It’s easier than forming an LLC, we promise!

When Not to Add an Additional Insured

Not every situation calls for additional insureds. Here are some examples of when not to add someone to your policy:

- When there’s no written contract

- When requested by unrelated third parties (like a business that isn’t directly involved)

- When a third party just needs to see proof of your insurance (send your COI)

- For expired or completed relationships (to prevent liability complications)

- For friends or family members helping your business

Rule of thumb: If someone else could be pulled into a claim because of your work, they probably need to be listed as an additional insured. If not, they might just need to see proof of your coverage.

Easy Additional Insureds in 3, 2, 1…

You started your small business to turn your passion into profits, not to stress over complicated additional insureds. That’s why Insurance Canopy makes it super easy to add qualified third parties to your policy.

Get an instant COI with additional insureds, send it off to whoever needs to see it, and keep your business moving forward. Our modern approach to insurance allows you to edit coverage online, right from your mobile phone or tablet, so you never miss an opportunity.

Show partners you’re a smart, safe business by tackling your next AI request like a pro.

FAQs About When to Add Additional Insureds

What Is an Additional Insured vs. a Certificate Holder?

An additional insured is covered by your policy for claims related to your work; a certificate holder simply receives a copy of your certificate of insurance.

What’s the Difference Between a Blanket vs. a Scheduled Additional Insured?

A blanket additional insured covers any party you’re required to add by contract. A scheduled additional insured is specifically listed by name on your policy (more common, with clearer terms).

How Fast Can I Get a Certificate of Insurance With Additional Insured Wording?

With Insurance Canopy, you can get a COI that lists your additional insureds in under 10 minutes, completely online. Learn how to get a COI for your business.

Will Adding an AI Raise My Premium (or Risk)?

The cost to add an additional insured on a small business policy depends on your industry, but many Insurance Canopy policyholders enjoy free additional insureds. For our other policies, additional insureds cost around $10–$15 annually, providing peace of mind for you and the parties you work with for just a few dollars a month.

Adding additional insureds doesn’t increase your risk — it helps protect your business and prepares you to land more opportunities. But, be aware that the more additional insureds you name, the more your coverage limits are shared.

What Are Common Mistakes When Adding Additional Insureds?

Some common mistakes when adding additional insureds are:

- Adding parties who have not requested AI status

- Adding yourself, your employees, friends, or family members as AIs

- Forgetting to remove AIs once the business relationship has ended

- Not verifying the correct name or address of AIs on the certificate of insurance

Need help adding an AI? Our friendly, licensed team is ready to walk you through the process and answer any questions. Contact us!

Kyle Jude | Program Manager

Kyle Jude is the Program Manager for Insurance Canopy. As a dedicated program manager with 10+ years of experience in the insurance industry, Kyle offers insight into different coverages for small business owners who are looking to navigate business liability insurance.

Kyle Jude is the Program Manager for Insurance Canopy. As a dedicated program manager with 10+ years of experience in the insurance industry, Kyle offers insight into different coverages for small business owners who are looking to navigate business liability insurance.