Let’s be real: shopping for business insurance is not fun. But if you’re serious about protecting all you’ve built, you gotta do it. Browsing insurance websites endlessly can make anyone feel dizzy (how many times can you read “peace of mind”?), so we’re here to make it super easy.

Here’s what to look for when choosing business insurance:

- Financial strength

- Customer reviews

- Coverage fit

- Claims and service

- Digital tools

These five key factors set the best small business insurance providers apart. Focus on these using our handy small business insurance scorecard to find your best choice.

Small Business Insurance Scorecard

How to Compare Small Business Insurance Easily

| Category | What to Look For | My Score (1–5) |

|---|---|---|

|

Financial Strength

|

A.M. Best rating of A- or higher

|

|

|

Customer Reviews

|

Low complaint ratio and overwhelmingly positive reviews

|

|

|

Coverage Fit

|

Tailored to your industry and customizable for your unique risks

|

|

|

Claims & Service

|

Fast and fair claims process supported with real human help

|

|

|

Digital Tools

|

Easy online policy management with instant COIs and additional insureds

|

|

Not sure what coverage to look for? Start with our guide: What Kind of Insurance Small Businesses Need.

Financial Strength: The Foundation of Trust

What If: Your insurer can’t pay out a covered claim.

Can you imagine the bind you’d be in if your insurance company didn’t have the funds to cover your losses? When you hear “financial strength” in an insurance context, that refers to a provider’s ability to pay claims.

Insurance companies often tout their financial strength ratings on their websites — typically represented by letter grades, like “A”, “B”, or “C” ratings. This means an independent agency has reviewed and scored that company based on its overall financial stability.

A strong financial strength rating means you can depend on your insurer even if there’s a widespread disaster or economic downturn. That rating says, “We’ve been vetted, and you don’t just have to take our word for it!”

One of the most common agencies you’ll see when comparing small business insurance is AM Best. An example rating from this agency is “A-”, which means an “excellent” ability to meet financial obligations on time.

What to Look For:

- Find the official ratings published on the agency’s website

- Verify the rating’s meaning based on the specific agency’s scale

- Insurers who don’t list their ratings or carriers are a red flag

For example, go to the insurer’s website. Find their financial strength rating (sometimes in the fine print in the footer) and carrier (if applicable). Navigate to the agency’s website and confirm the rating. Some insurance company names sound similar, so double-check the formatting to make sure you have the right provider.

How to Score:

⭐ 5: Has A- or higher rating and publishes it clearly

⭐ 3: Rated, but not easily verified

⭐ 1: No rating or unclear backing

Psst. Insurance Canopy policies are backed only by carriers rated “A-” and higher. Your coverage is as reliable as you, the business owner who gets things done.

Customer Reviews and Reputation: Real Proof

What If: You choose insurance based on a provider’s slick marketing, but you’re in for a rude shock when you check what customers actually say about their experience.

Is an insurance company actually meeting its policyholders’ needs? Your fellow small business owners will tell it to you straight. If there are hidden fees or if it’s impossible to speak with a real person for help, these issues show up in customer reviews.

Read up on what others have to say, especially noting things that are important to you, like transparent communication or how easily you can get a certificate of insurance (COI).

Small business insurance companies may curate the reviews that appear on their homepage, meaning these snippets won’t paint the whole picture. It’s best to navigate to an independent review page to get an unfiltered view of customer testimonials.

How to Check a Small Business Insurance’s Reputation:

- Go to their Google Reviews page

- Read through recent reviews to see what customers say

- Filter for the lowest or highest ratings for a comprehensive overview

- Click on suggested keywords like “additional insured” to narrow your search

- Take note of how the insurer responds to positive and negative reviews

- Look for reviews written by customers in your industry

Another crucial step is checking out the provider’s “About Us” page to see how long they’ve been in business and how many active policyholders they have. Higher numbers are a sign that they know what they’re doing!

How to Score:

⭐ 5: Consistently great reviews and low complaint ratio

⭐ 3: Mixed feedback or limited transparency

⭐ 1: Frequent unresolved complaints or poor reviews

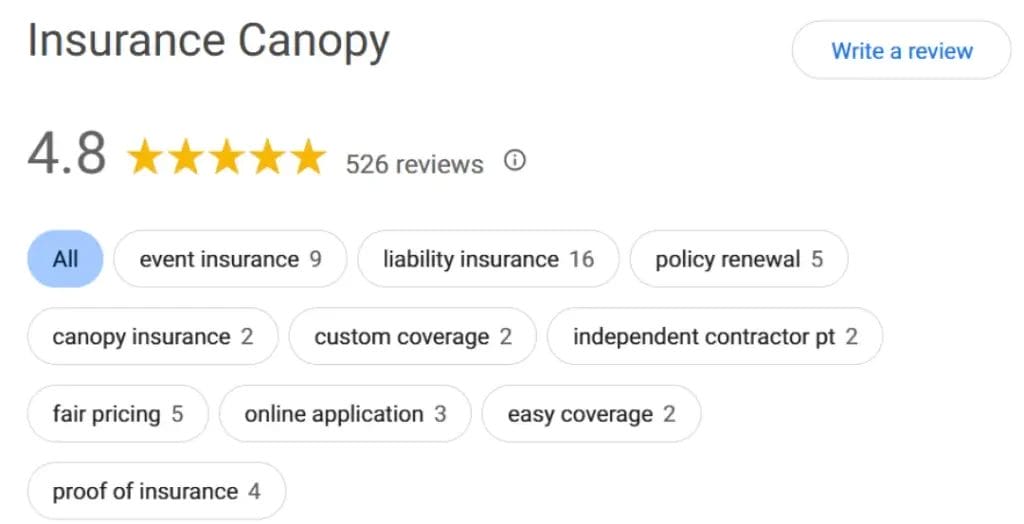

By the way… Insurance Canopy’s nearly 5-star Google rating and 15+ years serving over 135,000 small businesses mean other entrepreneurs really like us.

Coverage Fit: Protection Tailored to Your Business

What If: Your coverage is a generic package that doesn’t match your specific risks.

Small business insurance isn’t one-size-fits-all, so it’s crucial to ensure a perfect coverage fit. Your business is unique in what it offers and where it needs protection — that’s why your policy must be tailored to your specific needs.

For example:

- Personal trainer insurance must include professional liability coverage (their risk of client injury due to their workout advice is higher)

- Event vendor insurance is often packaged as short-term general liability coverage to meet organizer requirements

- Art vendor insurance should include product liability coverage (handmade goods are considered “riskier” because of the potential for injury)

What to Look For:

- An insurer that specializes in your niche

- Pre-packaged policies created for your industry risks

- Coverage limits that meet or exceed the industry standards

- Customizable coverage with tailored add-ons (like for your tools or cyber liability)

- Industry-specific explainers on what coverage you need and why

- Understanding how different types of business insurance work together can help you compare coverage options and avoid gaps in protection.

How to Score:

⭐ 5: Offers customizable, industry-specific coverage

⭐ 3: Some flexibility, but unclear exclusions

⭐ 1: One-size-fits-all or unclear what’s covered

Guess what? Insurance canopy offers thoughtfully designed coverage for 400+ business types, with optional add-ons to build your ideal policy. See who we cover.

Claims and Service: When Your Pick Really Matters

What If: Filing a claim becomes the worst experience of your life — the process is unclear, and you have to wait forever to hear from your insurer.

The hope is that you never have to actually use your insurance. But when a customer gets injured or claims you damaged their property, you need to file a claim and get back to business. The real test of an insurer provider is how they respond after something goes wrong.

Will your insurance company support you when it really counts?

What to Look For:

- An easy, online claims-filing process

- Quick claim acknowledgment (1–2 business days)

- U.S.-based agents who walk you through the next steps

- Consistent follow-up until resolution

Scoring an insurer based on its claims process is trickier because you won’t be able to see a set score of how often they pay out for covered claims or how satisfied customers are with the process. So, here are some other ways to verify their claim performance:

- Read through verified reviews specifically regarding claims

- Check if they have a dedicated “File a Claim” page with clear instructions

- Ensure there’s an option to track your claim online

- Ask your agent directly about their claims process

How to Score:

⭐ 5: Easy online filing, fast response, helpful support

⭐ 3: Basic claims info but limited follow-up

⭐ 1: Complicated or unresponsive claims process

Green flags ahead! Insurance Canopy’s non-commissioned, U.S.-based agents are dedicated to helping you through claims. We speak English and Spanish and are on standby to assist.

Digital Tools: Modern Coverage Built for Now

What If: You’re trying to grow your small business but are bogged down by a painfully slow, paper-heavy insurance process.

Today, there is simply no reason your insurance shouldn’t be fast and effortless. The best small business insurers make protecting your business easy with online tools accessible right from your mobile device. When you’re on the go, your coverage should be, too.

What to Look For:

- Instant online quotes

- Mobile policy dashboards

- Editable proof of insurance (COIs)

- Quick additional insureds

- Automatic policy renewal

- Online claims filing

- Monthly or annual payment options

- Customer support via chat, phone, or email

- Industry awards for insurance tech innovation

How to Score:

⭐ 5: Full digital access and instant documentation

⭐ 3: Some online tools, but limited automation

⭐ 1: Requires phone calls or manual paperwork

You should know… Insurance Canopy’s digital tools make it easy to quote, buy, renew, and download proof of insurance in minutes — anytime, anywhere. Plus, our parent company, Veracity Insurance, was named one of the world’s top fintech companies by CNBC in 2025.

Build Your Small Business Insurance Scorecard

Insurance Canopy Scorecard

| Category | What to Look For | My Score (1–5) |

|---|---|---|

|

Financial Strength

|

A.M. Best rating of A- or higher |

5 |

|

Customer Reviews

|

4.8/5 stars out of 509 Google Reviews |

5 |

|

Coverage Fit |

Tailored for small businesses, covering 400+ business types

|

5 |

|

Claims & Service |

Transparent claims process with an estimated 1–3 weeks until resolution and payout for covered losses |

5 |

|

Digital Tools

|

Easy online policy management and a global fintech award granted to our parent company

|

5 |

Pro Tip: Explore an overview of your best small business coverage options with our blog: The Best Small Business Insurance Providers Compared.

Insurance Canopy for Every Small Business

Here at Insurance Canopy, we believe protecting your small business should be easier than a weekly inventory check or calculating your next promo discount.

Now that you know how to choose business insurance confidently, do your research — we’ll be here to support you with top-rated coverage (and all the extras!) when you’re ready.

FAQs About How to Compare Insurance Providers

Which Matters More: AM Best Rating or Price?

In the long run, an insurer’s AM Best rating matters more when it comes to protecting your small business. A good financial strength score means your insurer can pay for your covered claims. Ideally, your coverage should strike a balance between affordability and dependability.

How Do I Verify a Provider’s Financial Strength?

Verify a provider’s financial strength by searching their exact name on the independent agency’s website. This will yield their financial strength score — check what it means (i.e., “A” equals “excellent”) in their official score guide.

How Do I Check an Insurer’s Complaint History?

Check an insurer’s complaint history by searching for it on the NAIC (National Association of Insurance Commissioners) database. There, you can find a score based on the number of complaints they receive compared to their size.

Only licensed carriers will show up in this complaint index (not producers or managing general agents).

Will Choosing the Cheapest Insurance Option Hurt Me at Claim Time?

Choosing the cheapest insurance option can backfire at claim time if the policy lacks value (for example, coverage limits that are too low). It’s essential to compare coverage based on multiple factors, including financial strength, claims history, and customer support.

The best policy meets all of your insurance scorecard criteria at an affordable price.

Which Endorsements Do Clients Commonly Ask For?

Clients commonly ask for insurance endorsements like:

- Additional insureds

- Waiver of subrogation

- Primary and non-contributory wording

- Per-project or per-location aggregate limits

If you’re unsure about an endorsement request, our licensed agents are happy to help! Contact us and we’ll walk you through the process.

Kyle Jude | Program Manager

Kyle Jude is a Program Manager at Insurance Canopy, where he helps design and maintain liability coverage for small business owners. With 10+ years of experience in the insurance industry, he works closely with carriers, underwriters, and compliance teams to ensure coverage remains accurate, responsive, and aligned with real-world risks.

Kyle Jude is a Program Manager at Insurance Canopy, where he helps design and maintain liability coverage for small business owners. With 10+ years of experience in the insurance industry, he works closely with carriers, underwriters, and compliance teams to ensure coverage remains accurate, responsive, and aligned with real-world risks.