How Do I Get a Certificate of Insurance (COI) and Add an Additional Insured?

Get copies of your COI and add additional insureds to your policy anytime through your online user dashboard.

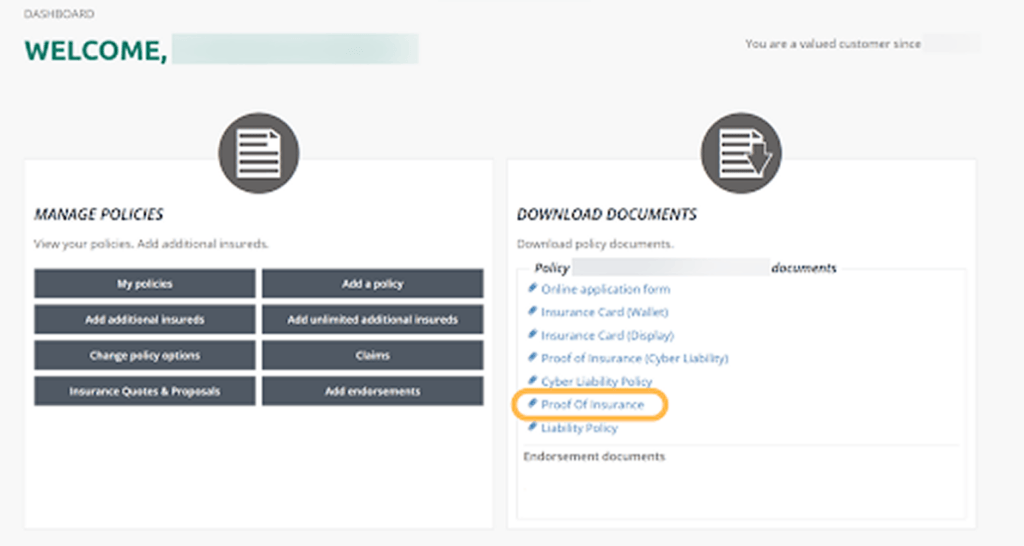

To get your COI, simply log in to your account and click on “Proof of Insurance” under the “Download Documents” section. Or, click on “My Policies” and select “Proof of Insurance” under “Download Documents

To add an additional insured after you’ve already purchased a policy, navigate to the “Manage Policies” section and click on “Add additional insureds.”

Does Cleaning Liability Insurance Cover My Employees?

Are 1099 or Contract Workers Protected by My Policy?