Gardening Business Insurance Cost

Understanding your gardening business insurance costs makes it easier to plan your budget and protect your livelihood from accidents, equipment loss, or lawsuits.

Insurance Canopy offers affordable, customizable coverage options designed specifically for gardeners, so you get the protection you need to protect and grow your business.

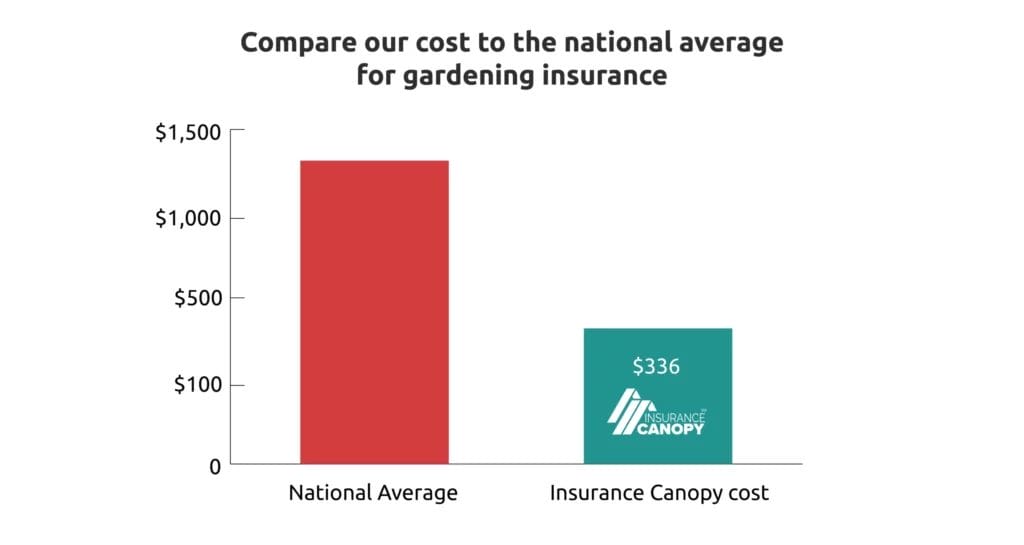

How Much Is Gardening Insurance?

Gardening insurance with Insurance Canopy starts at just $31 per month or $336 per year. Insurance Canopy offers competitive rates so you can spend more of your hard-earned revenue on scaling your business, not paying high insurance premiums.

How Employee Count Affects Pricing

The more people you have planting, digging, and hauling, the more coverage you’ll need, which can raise your premium. Why? More employees mean a higher chance of workplace injuries, property damage, or accidents that your policy might need to cover.

Here’s a quick breakdown:

| # of Employees | 500k /1M Premium + Fees | 1M / 2M Premium + Fees |

|---|---|---|

|

Owner + 1-2 Employees |

$375 / $31.25 per month |

$450 / $37.50 per month |

|

3 Employees |

$480 / $40 per month |

$580 / $48.33 per month |

|

4 Employees |

$585 / $48.75 per month |

$710 / $59.16 per month |

|

5 Employees |

$690 / $57.50 per month |

$840 / $70 per month |

|

6 Employees |

$795 / $66.25 per month |

$970 / $80.83 per month |

|

7 Employees |

$900 / $75 per month |

$1,100 / $91.66 per month |

|

8 Employees |

$1,005 / $83.75 per month |

$1,230 / $102.50 per month |

|

9 Employees |

$1,110 / $92.50 per month |

$1,360 / $113.33 per month |

Most Popular Gardening Insurance Policies (+ Their Cost)

Gardening professionals typically choose a mix of insurance policies to protect their business, equipment, and employees. Knowing the typical costs of these coverages improves your budget practices and keeps your business financially protected when the unexpected happens.

| Coverages | Our Lowest Price | Industry Average |

|---|---|---|

|

General Liability Insurance |

$336 per year |

$550 per year |

|

Trailer and Equipment Insurance |

$155 per year |

$350 per year |

|

Workers Compensation |

$1,141.86 per year |

$1,627 per year |

|

Commercial Auto Insurance |

Rates vary |

$1,588 per vehicle per year |

|

Landscaping Bonds |

Rates vary |

Ranges from 1% to 15% of the total bond amount |

|

Additional Insureds (AIs) |

$10 per year per AI |

$25 per month |

|

Cyber Liability Insurance |

$99-$150 per year |

$260 per year |

**Based on the median cost of policies for landscaping insurance bought with Insurance Canopy.

General Liability Insurance

If a client trips over a bag of soil you left near the walkway, or you accidentally knock over their potted lemon tree while working, general liability insurance can cover medical costs, property repairs, and legal fees.

| Coverage | Lowest Annual Cost / Lowest Monthly Cost |

|---|---|

|

$500K Per Incident / $1M Per Year |

$336 / $30.50 |

|

$1M Per Incident / $2M Per Year |

$411 / $36.75 |

| Limits (Occurrence / Aggregate) | Lowest Annual Cost / Lowest Monthly Cost |

|---|---|

|

$5,000 |

$155.00 / $12.92 |

|

$10,000 |

$258 / $21.50 |

|

$25,000 |

$670 / $55.83 |

Trailer and Equipment Insurance

From pruning shears to wheelbarrows and your trusty tiller, your tools are the backbone of your business. Trailer and equipment coverage, also known as inland marine insurance, covers replacement or repair fees if they’re stolen or damaged, so you can keep gardening without missing a season.

Workers Compensation

Gardening can be hard on the body. If someone on your team gets hurt on the job, workers compensation is designed to pay for their medical care and replace some of their lost wages while they recover. It’s protection for your crew and peace of mind for you.

Exact coverage depends on your state, but common limits include:

Because workers compensation laws differ from state to state, your coverage limit depends on your state’s specific statutory requirements.

Employers’ Liability Coverage Limits

The maximum coverage for damages resulting from bodily injury by disease for any number of employees.

$1,000,000 Policy Limit

The maximum coverage for bodily injury to one or more employees in any one accident.

$1,000,000 Each Accident

The maximum coverage for damages resulting from bodily injury by disease for any number of employees.

$1,000,000 Each Employee

Commercial Auto Insurance

Your business vehicle is more than just transportation – it’s your mobile garden shed. Whether it’s loaded with flats of flowers, bags of mulch, or your favorite tools, accidents can happen on the way to a job site. Commercial auto insurance helps cover:

- Fixing or replacing your work vehicle

- Medical costs if someone gets hurt

- Repairs to other people’s property

- Legal expenses if you’re sued

Heads up: Your regular personal car insurance probably won’t cover accidents that happen while you’re working. That’s why having commercial auto insurance is a smart move to keep you covered.

Landscaping Bonds

Some clients or local governments might require a bond before you can start work. A gardening bond is like a promise that you’ll finish the job as agreed and follow any rules or regulations.

If something goes wrong and a claim is filed, the bond company will pay the client. But your business will need to pay the bond company back. Using bonds for your business shows clients you’re trustworthy and serious, making it easier to land bigger jobs.

Types of gardening bonds include:

- License and permit bonds: Some states or towns require these to make sure your gardening business follows local laws and regulations

- Contractor bonds: Protects your clients if a landscaping or planting job isn’t finished the way you promised

- Business service bonds: Cover clients if an employee takes tools, plants, or money while working on their property

Additional Insureds

When you add an additional insured (AI) to your gardening policy, you’re extending certain protections to another party (like a property manager or event organizer) who could be named in a claim because of your work.

Imagine you’re hired to install raised garden beds at a senior living community. During the job, a resident trips over a wheelbarrow and gets injured. Even though your business is responsible, the community’s management could still be included in the lawsuit. Listing them as an additional insured means your policy can cover claims tied to your services.

Most botanical gardens, homeowners associations (HOA), and commercial properties require you to add them as an AI before doing on-site gardening work. With Insurance Canopy, you can add additional insureds anytime from your customer dashboard.

Price per additional insured: $10 per year

Cyber Liability Insurance

Even gardening businesses face online threats. If you store client contact details, take bookings through your website, or accept digital payments for your services, you could be a target for cybercrime. Cyber liability insurance protects you from the financial fallout.

It can cover costs like:

- Data breach notifications if your booking system is hacked

- Loss of customer data, like addresses or payment details

- Ransomware or cyber extortion demands payment to unlock your files

- Legal fees if affected clients sue you

- Business interruption expenses if your website or payment system goes down

| Coverage Option 1 | |

|---|---|

|

Premium |

$8.25 / month $99 /year |

|

Deductible |

$1,000 |

|

Coverage |

Aggregate Claims-Made Liability: $100,000 Cyber Event Costs: $25,000 Ransom Loss: $10,000 Cyber Deception: $10,000 |

| Coverage Option 2 | |

|---|---|

|

Premium |

$12.50 / month $150 /year |

|

Deductible |

$1,000 |

|

Coverage |

Aggregate Claims-Made Liability: $250,000 Cyber Event Costs: $50,000 Ransom Loss: $10,000 Cyber Deception: $10,000 |

What Affects Your Gardening Business Insurance Cost?

The cost of your gardening insurance depends on how you run your business and the unique risks involved. For example, installing irrigation systems or working with heavy landscaping equipment poses a higher risk than seasonal flower bed maintenance, which can affect your premiums.

Other important factors include:

Services offered

Other maintenance jobs like pool maintenance, tree trimming, pressure washing, and snow and ice removal (for the winter months)

Business size

Having more employees means more potential for workplace injuries, which increases your workers compensation and liability costs

Equipment value

High-end tools like commercial mowers or specialized pruning gear increase your equipment insurance premiums

Claims history

If you’ve had recent accident or property damage claims, insurers see you as a higher risk and may charge more

Tips for Saving on Landscaping Insurance

Gardening is seasonal and sometimes unpredictable, but your insurance costs don’t have to be. Here are tailored tips to keep premiums affordable without sacrificing protection:

Bundle policies

Combine your general liability, equipment, and cyber coverage with one insurer like Insurance Canopy to save money and simplify renewals

Pay annually

Since many gardening businesses operate seasonally, paying your full premium upfront can earn you significant discounts compared to monthly payments

Keep claims low

Use clear signage, secure your tools overnight, and follow safety best practices to avoid accidents that can raise your rates

Get Growing With Instant Protection From Insurance Canopy

Insurance Canopy makes it easy to protect your gardening business with affordable, customizable coverage. Apply online, choose your policies, and download your certificate of insurance (COI) instantly.

Common Questions About Gardening Business Insurance Costs

Is Gardening Insurance Required?

Gardening insurance may be required based on your state, city, or client contracts. Many HOAs, botanical gardens, and commercial properties require proof of insurance before hiring you.

Can I Get Insured if I’m a Part-Time Gardener?

Yes, you can get insured if you’re a part-time gardener. Insurance Canopy offers coverage for seasonal, part-time, and full-time gardening businesses so you can stay protected no matter your schedule.

What Does Gardening Insurance Typically Cover?

General liability insurance for gardeners covers third-party injuries, property damage, and related legal costs, such as:

- Breaking a customer’s sprinkler system

- A passerby tripping over your tools

- Making false claims about competitors in your advertising materials

From there, you can customize your policy with add-ons like equipment protection, workers comp, commercial auto, cyber liability, or additional insureds – giving you the flexibility to match your coverage to how you work.

Khaleel Hayes | Copywriter

Licensed insurance agent in the state of Colorado and fully trained in Insurance Canopy coverage, copywriter Khaleel Hayes writes about DJ and Entertainer policies and products. He holds a B.A. in Journalism from Metropolitan State University of Denver. Before working at Veracity, Hayes worked as an Amazon warehouse worker, a B2B writer for software consultancy SelectHub, and a freelancer for numerous publications in the Mile High City.

Licensed insurance agent in the state of Colorado and fully trained in Insurance Canopy coverage, copywriter Khaleel Hayes writes about DJ and Entertainer policies and products. He holds a B.A. in Journalism from Metropolitan State University of Denver. Before working at Veracity, Hayes worked as an Amazon warehouse worker, a B2B writer for software consultancy SelectHub, and a freelancer for numerous publications in the Mile High City.

Kyle Jude | Program Manager

Kyle Jude is the Program Manager for Insurance Canopy. As a dedicated program manager with 10+ years of experience in the insurance industry, Kyle offers insight into different coverages for small business owners who are looking to navigate business liability insurance.

Kyle Jude is the Program Manager for Insurance Canopy. As a dedicated program manager with 10+ years of experience in the insurance industry, Kyle offers insight into different coverages for small business owners who are looking to navigate business liability insurance.