Whether you’re a weekend craft fair regular, a full-time food truck owner, or a wedding DJ with a packed summer schedule, vendor insurance is a must-have. The right policy can protect your business and your peace of mind, without blowing your budget.

What’s the Real Risk of Choosing the Wrong Insurance (or None at All)?

Going without vendor insurance or having the wrong type of coverage can put your small business at serious risk. We’re talking:

- Canceled contracts

- Expensive lawsuits

- Out-of-pocket losses

- Denied access to events

Most venues and event organizers require liability insurance before you can show up. Without it, you could be turned away at the door — or worse, left on the hook for thousands of dollars if something goes wrong.

What Are You Actually Protecting Yourself From?

Think of vendor insurance as your safety net that has your back. With it, you’re commonly covering:

- Injuries – A customer trips at your booth or slips near your setup

- Property damage – You accidentally damage the venue’s floors, walls, or electrical systems

- Legal help – Your policy can help cover attorney fees and settlements from covered incidents

- Product issues – Someone claims your product caused them harm or made them sick*

- Stolen or damaged gear – Optional coverage helps protect your gear from accidents, theft, or event mishaps

Understanding what you’re trying to protect against makes it easier to choose a policy that fits your exact needs (and budget).

*Coverage available on annual policies only.

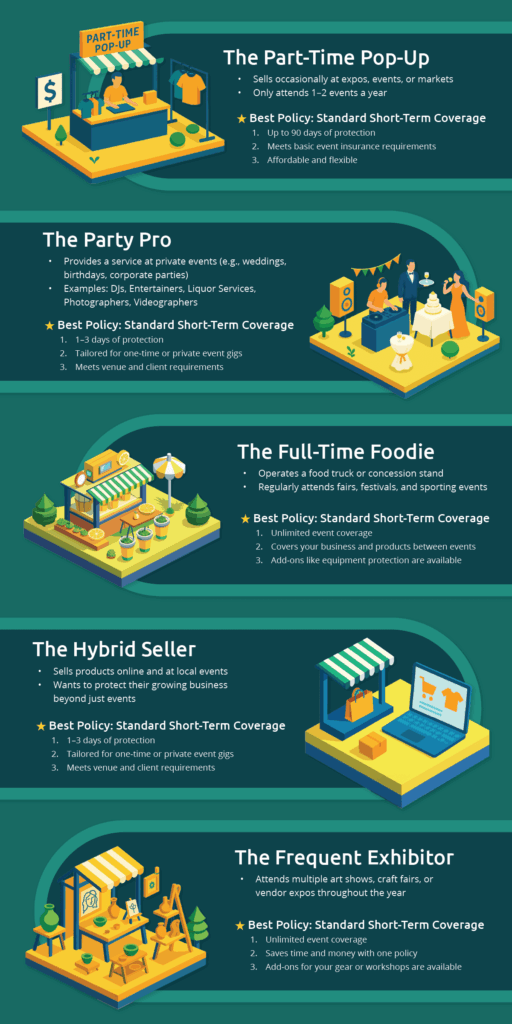

Match the Coverage to the Way You Work

Not all vendors are cut from the same (table)cloth. Some pop up at craft fairs once a year, while others are booked every weekend, rain or shine. Your insurance should flex to match the way you do business.

Use this quick guide to find the best coverage based on how (and how often) you work.

Vendor Insurance Must-Haves Checklist

Here’s your go-to checklist to make sure your vendor insurance covers the essentials:

- $1M per occurrence /

- $2M aggregate limits

- Downloadable vendor Certificates of Insurance

- Flexible terms (single event or annual plans)

- Add-ons for tools, gear, or product liability

- No hidden fees or confusing jargon

- Ability to add other parties as additional insureds

Learn More: Vendor Insurance Types & Requirements

Avoid These Common Insurance Mistakes

Even seasoned vendors slip up and miss a detail now and then. With a little know-how, you can dodge these pitfalls:

- Getting too little coverage – General liability only covers accidents that happen from business operations (like running a booth), so you may want to opt for a policy with product liability if you sell food or handmade goods

- Getting too much coverage – Only doing a couple of events a year? You might not need an annual policy.

- Forgetting to add additional insureds – Many venues, cities, and event organizers require this, so forgetting to add them may result in a failure to comply with event rules, and you forfeiting your vendor spot

- Buying last minute – Not all providers offer an instant proof of coverage, which may lead to rush fees or failure to show your Certificate of Insurance before an event begins

What Does Vendor Insurance Cost?

Our base vendor policy starts at $49, giving you the standard short-term coverage required to attend most events. It’s more affordable than you might think!

Different types of vendors may require different types of coverage, so your total premiums may vary depending on factors like:

- Policy length (short-term vs. annual)

- Type of work (food vendor vs. photographer vs. craft seller)

- Optional add-ons (equipment protection, cyber liability, etc.)

- Location and number of events

For example, a one-day event might cost less than a full-year policy. But don’t fall into the trap of thinking cheaper is always better. You get what you pay for, so consider what’s actually covered in each plan.

| Event Frequency | Best Policy Type | Why It Works |

|---|---|---|

|

One-time or occasional |

Short-term Vendor Policy |

Budget-friendly, single-event coverage |

|

Regular or frequent |

Annual Vendor Policy |

Covers you all year, one-time purchase |

Pro Tip: If you attend more than 4–6 events per year, go for an annual policy. It typically saves you money and saves you from the last-minute scramble before every show.

How to Get Insured Fast (Step-by-Step)

Worried the process will take forever? Don’t sweat it! Here’s a quick step-by-step guide that’s quicker than popping open an E-Z Up:

- Apply online in five minutes or less

- Choose your coverage by selecting a policy that best fits your needs, a start date, and any optional coverage (if you choose an annual plan)

- Provide some basic details about yourself and your business

- Review your coverage details and submit your payment online

- Get your Certificate of Insurance within minutes of your purchase!

In a matter of minutes, you’ll be ready to show up at your next event fully protected.

FAQs About Choosing the Right Vendor Insurance

Do I Need Vendor Insurance for Just One Event?

Yes, you may need vendor insurance for just one event since many organizers and venues require vendors to carry liability insurance.

A short-term vendor insurance policy is an easy, affordable way to meet those requirements and protect your business from unexpected risks without the annual commitment.

What’s the Difference Between Vendor Insurance and General Liability Insurance?

Vendor insurance includes general liability coverage, but it’s tailored specifically for small business owners, artists, food vendors, and service providers working at events.

General liability insurance is a broader policy for businesses operating full-time, while vendor insurance is typically shorter-term and event-specific, with options for annual coverage if you attend events regularly.

What if the Event Organizer Asks to be Listed as “Additional Insured”?

If the event organizer asks to be listed as an additional insured, you can easily add them for little or no cost! You can add a third party to your policy as an additional insured when you are buying a policy, or add them to an existing policy from your online dashboard at any time.

This protects the event host if a claim is made involving your booth, service, or products. Always check the event’s insurance requirements so you can include them when buying your policy.

Can I Buy Vendor Insurance the Day Before (or on the Day of) My Event?

Yes, you can buy vendor insurance the day before or on the day of your event! With same-day coverage, your policy can begin today and last up to three days. Just make sure to allow enough time to get your vendor Certificate of Insurance in hand before setup.

For example, if you’re working in someone else’s space and an accident happens because of your actions, they’ll be covered. But if something unrelated to your work (like a broken pipe) happens on their property, they’ll need their own coverage.

Is Product Liability Included in Vendor Insurance?

No, product liability is not included in short-term vendor insurance policies. If you sell physical goods (especially food, skincare, or wellness products), consider an annual vendor insurance policy with product liability included in the base policy.

Does Vendor Insurance Cover My Gear or Booth Setup?

No, vendor insurance does not cover your gear or booth setup. Vendor insurance covers your liability if your booth causes harm or damage to others.

To cover your equipment, tools, or display items against theft, damage, or loss, you’ll want to add inland marine insurance to an annual policy.