Personal Trainer Insurance Cost

Wondering if the cost of personal trainer insurance is worth it? This breakdown explains how much you can expect to pay and what affects your price, so you can support clients with confidence.

How Much Does Personal Trainer Insurance Cost?

Personal trainer liability insurance costs as little as $15/month or $159/year with Insurance Canopy. This base policy is priced at a flat rate for all personal trainers, regardless of training style or experience level.

Your base policy includes essential coverages to protect against common claims that arise in your industry, such as client injuries or property damage.

- General Liability

- Professional Liability

- Personal and Advertising Injury

- Products and Completed Operations

- Damage to Premises Rented

- Medical Expenses

Every personal trainer works differently, so we offer coverage add-ons you can opt into. You only pay for additional coverages that make sense for your business protection.

- Gear and Equipment (Inland Marine) Coverage: +$1.33 – $10.67/month

- Sexual Abuse and Molestation (SAM) Coverage: +$10.33 – $14.46/month

- Diet and Nutrition Coverage: +$6.83/month

- Cyber Liability Coverage: +$8.25/month

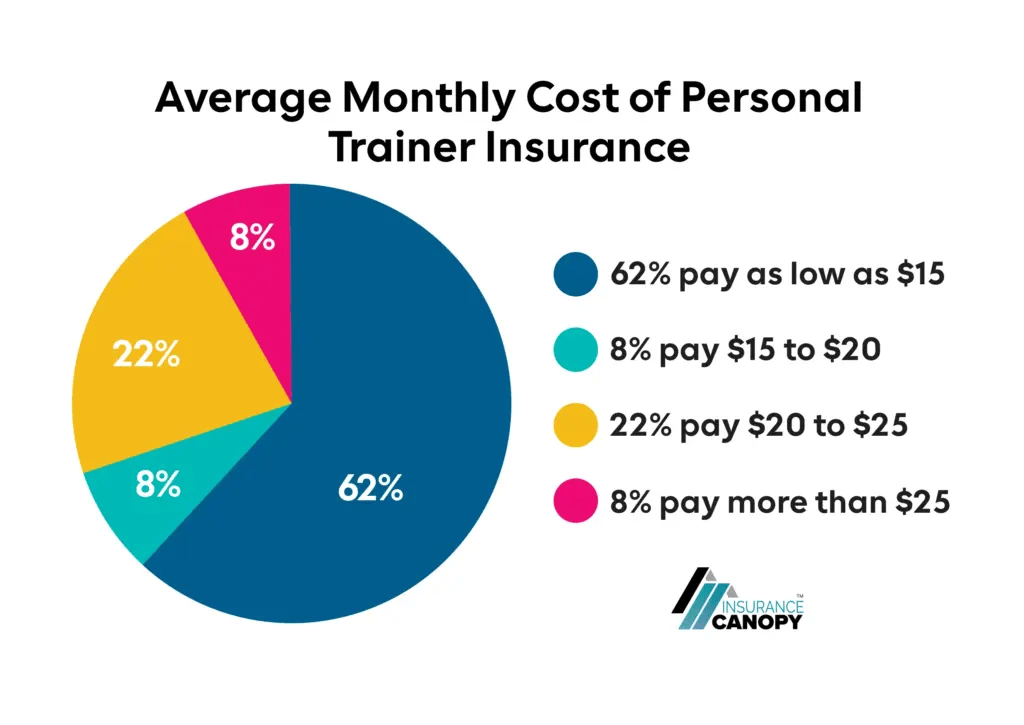

62% of personal trainers protect their businesses with a base policy (general + professional liability insurance) and pay just $15/month. 38% pay a little extra to enhance their protection with add-on coverages.

See more insights like these in our Personal Trainer Insurance Annual Data Report.

Data based on new policies purchased between October 2025 and March 2026.

What Types of Payment Plans Are Available?

Choose a payment plan that fits your budget calendar: monthly or annual.

Monthly payments

✔️ Base policy amounts to $180 in total for the year

✔️ Pay your insurance premium in monthly installments

✔️ Ideal for businesses with tighter cash flow

Annual payments

✔️ Base policy equivalent to $13.25/month when paid annually

✔️ Save up to 13% with one upfront payment

✔️ Enjoy a full year of peace of mind

How Much Does Each Coverage Cost?

General + Professional Liability: $15/month or $159/year

Can cover harm to clients or others due to your training and operations.

Examples:

- Client slip-and-fall injuries

- Injuries caused by your instruction

- Damage to the space you rent

- Damage to client property

Gear and Equipment (Inland Marine) Coverage: +$1.33 – $5.55/Month

Pays to repair or replace your movable business gear in case of theft or damage.

Sexual Abuse and Molestation (SAM) Coverage: +10.33/Month

Can provide coverage if a client alleges sexual misconduct, helping protect you against costly legal claims.

Diet and Nutrition Coverage: +$6.83/Month

Extends your liability coverage to include general nutrition advice.

Cyber Liability Coverage: +$8.25/Month

Helps your business recover from data breaches, such as the exposure of client information.

Additional Insureds: $15 Each | $30 Unlimited

Add gyms, studios, landlords, or other qualified third parties to your policy.

What Factors Affect Personal Trainer Insurance Price?

Typically, personal trainer insurance premiums are calculated by factors such as your fitness modalities, location, years of experience, and claims history. Insurance Canopy simplifies cost by basing it solely on two factors: your payment plan and any optional add-ons you select.

Choose to pay monthly or annually. An annual payment plan saves you in the long run!

Selecting optional coverages adds to your premium cost and strengthens your base policy.

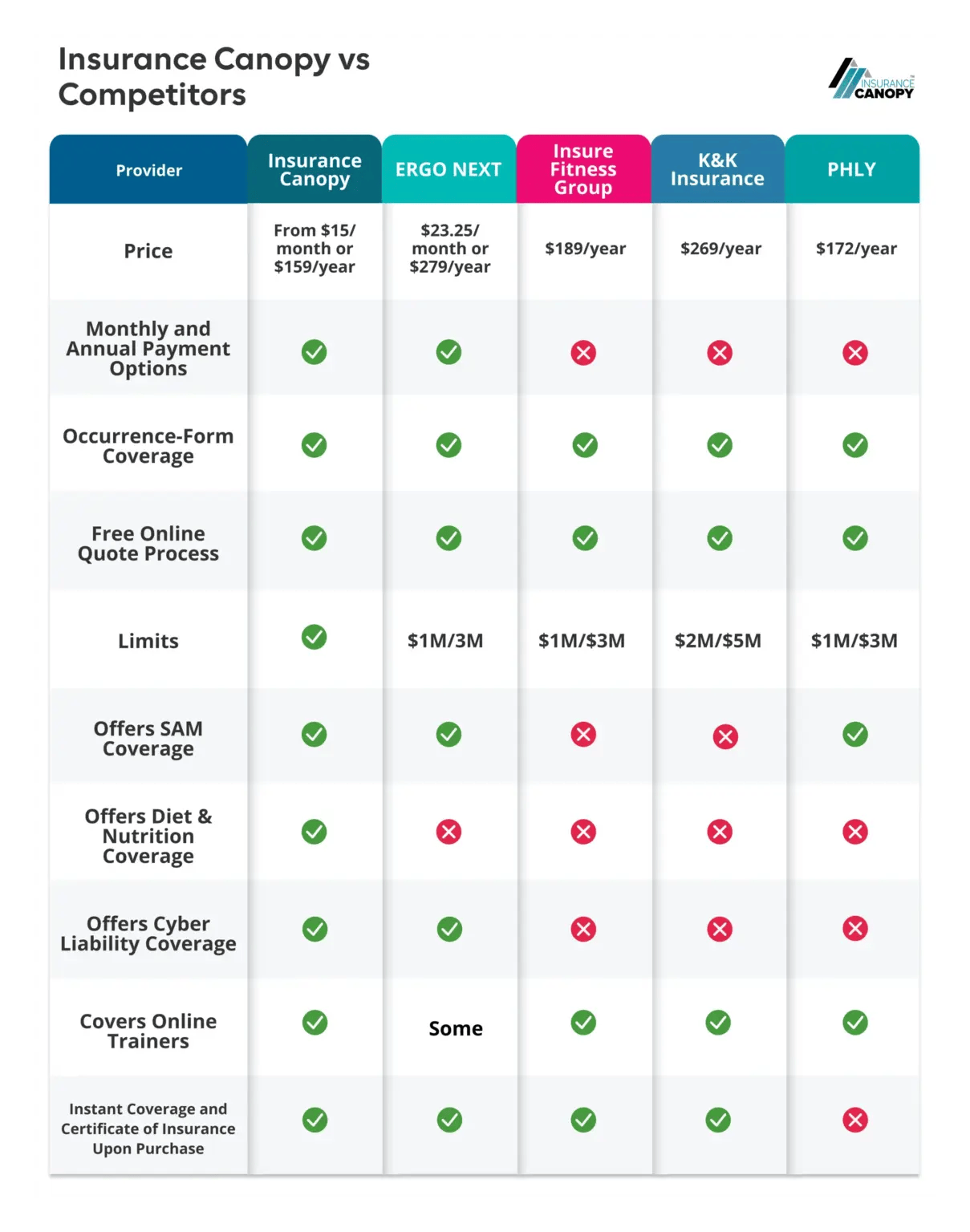

Personal Trainer Cost Comparison

Insurance Canopy is the top choice for affordable, top-rated personal trainer insurance — but see for yourself! Our comparison chart shows how we stack up against other policies on the market.

Note: All amounts shown were calculated based on a policy for a personal trainer working in Utah, USA. All data was collected from real insurance quotes provided by each competitor in March 2026.

Can I Reduce the Cost of My Insurance?

With Insurance Canopy, you can feel confident you’re protected with high coverage limits at truly competitive rates. Here are a few ways to keep your costs low.

Pay Upfront

Avoid extra monthly fees by paying for the full year of coverage upfront.

Consider Unlimited Additional Insureds

If you train out of multiple gyms, consider opting for $30 unlimited additional insureds, rather than adding them one at a time for $15 each.

Keep EZ Renew On

Avoid lapses in coverage (which expose you to paying for claims out of pocket) by toggling EZ Renew on.

Store Your Gear Safely

Claims for lost or stolen equipment include a deductible, meaning you pay a portion before coverage applies. Keeping your gear stored securely can help you avoid unnecessary expenses.

- Trusted by 12,000+ fitness pros

- Coverage for 100+ fitness modalities

- Instant certificate of insurance

- Customizable policy

- Free additional resources

- Occurrence-based coverage*

- Online and multi-location coverage**

- 24/7 online policy access

Coverage Details

General & Professional Liability

The most your policy can pay annually for bodily injury and property damage claims occurring during your coverage as a result of your business operations or professional services. For example, someone slips in your studio or is injured during a workout you were leading.

$3,000,000

General & Professional Liability Each Occurrence

The maximum the insurance carrier will pay for a bodily injury or property damage claim that you become legally obligated to pay due to your business and professional services.

$2,000,000

Products Completed Operations Aggregate

The maximum amount your policy will pay annually for claims of bodily injury or property damage due to an incident that occurred with a product during or after your class, such as a faulty piece of equipment injuring a client.

$3,000,000

Personal & Advertising Injury

The amount your policy will pay for claims arising out of one or more of the following offenses:

- False Arrest, detention or imprisonment

- Malicious prosecution

- Wrongful Eviction or Wrongful Entry

- Oral or written publications that slander or libels a person or organization

- Oral or written publication or material that violates a person’s right of privacy

- The use of another’s advertising idea in your advertisement

Included

Damage to Premises Rented to You

Applies to damage by fire to premises rented to the insured and to damage regardless of cause to premises (including contents) occupied by the insured for 7 days or less.

$300,000

Medical Expense Limit

A no-fault medical policy that allows you to cover medical or funeral expenses for an individual up to the issued limit without deducting from the general liability aggregate limit. The injury or death must be as a result of a bodily injury caused by business operations.

$ 5,000

Deductible

The amount we deduct from a claim before paying up to your policy limits.

$ 0

Gear & Equipment Coverage

Also known as “inland marine,” it covers property that is movable or transportable in nature (e.g. supplies, equipment, or inventory) but excludes coverage for structures and items that are a permanent part of the structure. There are multiple tiers of coverage to choose from, starting at $1.33/month with a $100 deductible per claim.

$1.33 – $10.67/month

Cyber Liability Coverage

The maximum amount paid out in the case of a cyber attack on your business. Because this coverage is not automatically included in the standard General Liability Policy, you will need to opt into this coverage. See the application for additional coverage details for Cyber Liability Insurance.

$8.25 – $12.50/month

Diet & Nutrition Coverage

Coverage for additional services you offer clients, such as diet guidelines, meal plans, or the sale/recommendation of health supplements. These services are not covered by professional liability and require Diet & Nutrition Coverage.

$6.25/month

Additional Insureds

Coverage for a third party, such as a business, property owner, event organizer, or employer who could be named in a claim arising from your business operations. It cannot be used for employees, friends or family, other trainers, yourself, or other businesses you may own. Add one additional insured for $15, or choose unlimited additional insureds for $30.

$1.25 – $2.50/month

Sexual Abuse & Molestation (SAM) Insurance

Coverage for defense costs if you’re wrongly accused of sexual harassment or improper conduct.

$10.33 – $14.46/month

How Do I Get a Quote?

Get covered in about 10 minutes! Start the checkout process, tell us about your business, and customize your policy. After purchase, you get instant access to your certificate of insurance — easier than building a workout plan.

FAQs About Personal Trainer Liability Insurance Costs

Why Do I Need Insurance?

Personal trainers need insurance to meet gym requirements for work. Beyond that, carrying liability coverage provides essential financial protection if a client is injured, their property is damaged, or they claim your instruction was negligent.

How Much Does Personal Trainer Insurance Cost Per Year?

With Insurance Canopy, personal trainer insurance starts from just $159/year. Your final cost is determined by your payment plan and any optional coverage add-ons you select.

Is Personal Trainer Insurance Expensive?

Personal trainer insurance can be surprisingly affordable! In fact, Insurance Canopy’s policy (from $15/month) is one of the lowest-priced options on the market, with industry-preferred limits of $2 million per occurrence and $3 million aggregate.

Does My Gym’s Insurance Affect My Cost?

Your gym’s insurance typically doesn’t affect your cost because it doesn’t cover you personally. Most gyms require you to carry your own policy, which protects you independently of their coverage.

How Is Online Trainer Insurance Priced?

Insurance Canopy’s coverage for online personal trainers is included in the same base price of $15/month (or $159/year). This means you can train clients both online and in person under one policy, without paying extra.

Still have questions regarding our policies? Feel free to reach out to our licensed insurance agents. We are available Monday through Friday from 8am–8pm ET.

JoAnne Hammer | Program Manager

JoAnne Hammer is the Program Manager for Insurance Canopy. She has held the prestigious Certified Insurance Counselor (CIC) designation since July 2004.

JoAnne understands that starting and operating a business takes a tremendous amount of time, dedication, and financial resources. She believes that insurance is the single best way to protect your investment, business, and personal assets.

JoAnne Hammer is the Program Manager for Insurance Canopy. She has held the prestigious Certified Insurance Counselor (CIC) designation since July 2004.

JoAnne understands that starting and operating a business takes a tremendous amount of time, dedication, and financial resources. She believes that insurance is the single best way to protect your investment, business, and personal assets.

*All customers who purchased a policy before 7/1/2024 will have a policy issued through Great American Insurance. This policy does not include occurrence form coverage and will be eligible to receive it after 7/1/2025.

**Currently not for sale in Missouri.