- Last Updated:

- 6/26/2024

- Chelsea Ramsey, ACE CPT

General Liability vs Professional Liability for Personal Trainers: What’s the Difference?

What is the difference between general liability and professional liability insurance for personal trainers?

The main difference is that general liability insurance is designed to cover bodily injury and property damage caused by your business operations, while professional liability insurance may specifically cover physical damages related to your personal training services.

AMRAP, EMOM, PR — you speak fluent fitness. But when you start hearing terms like “general” and “professional liability,” insurance can feel like a whole new language.

What’s the difference, and do you need both?

General and professional liability insurance cover different risks, and most personal trainers benefit from having both. Here’s how they work and how to choose the right personal trainer liability insurance, whether you offer 1-on-1 sessions, CrossFit coaching, small group classes, or other personal training and fitness styles.

What Liability Insurance Really Is

Personal trainer liability insurance is financial protection designed for instances when your fitness business harms someone else, such as a client. It’s a safety net that empowers you to train with confidence, because no matter how careful you are, there’s always a risk of things going wrong in fitness work.

The two main types of insurance personal trainers need are general and professional liability. Both coverages help protect your business from the most common claims you face as a personal trainer.

Let’s explore how they differ!

General Liability Insurance for Personal Trainers

General liability insurance is designed to cover everyday accidents that happen because you’re running your business, such as a client getting hurt or their belongings getting damaged during a session.

General liability insurance offers broad protection for the unexpected. If someone slips and falls, equipment fails and injures someone, or you accidentally damage the space where you train, this coverage can step in.

The keyword to note for this coverage is “general,” so think of accidents that may occur simply by you offering a training session. Now subtract what-ifs that are specific to your fitness instruction and advice — these fall under professional liability instead.

Examples of Personal Trainer General Liability Claims

Here are some examples of general liability claims for personal trainers.

- During a group Pilates class, a spilled drink causes a student to slip and break their wrist. They sue you because the injury happened in your class.

- At an outdoor boot camp, a client accidentally damages expensive park equipment. The park holds you responsible for repair costs.

- In a CrossFit class, an athlete drops a kettlebell that crushes another athlete’s new iPhone. The owner expects you to cover the replacement.

Real-World Claim Example

During a small-group training session in Massachusetts, a participant allegedly tripped over loose equipment left near the workout area and fell. She claimed the fall caused injuries and filed a claim against the trainer. Luckily, the trainer had insurance to help cover the cost of the claim.

Claim Payout: $45,000

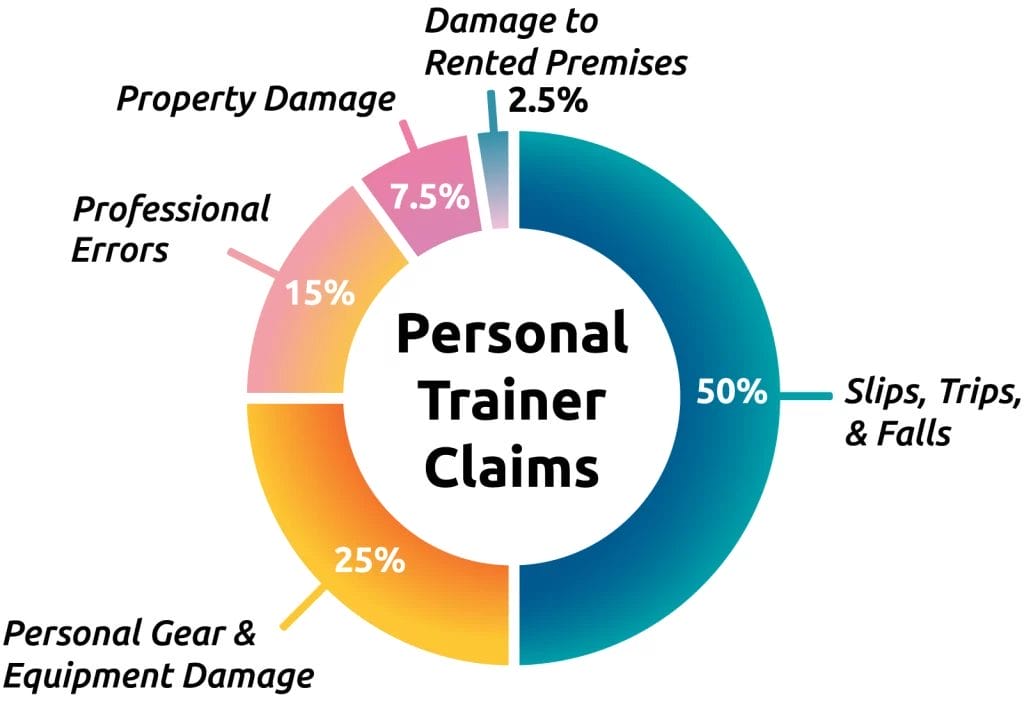

Accidents happen when you least expect them. According to our internal 2024 personal trainer claims statistics, about half of personal trainer insurance claims are for slip-and-fall injuries.

*Based on Insurance Canopy claims data from 2020-2024.

Professional Liability Insurance for Personal Trainers

Professional liability (errors and omissions) insurance is designed to cover claims related to your expertise (instruction, programming, and advice) if it leads to a client’s physical injury.

Professional liability insurance focuses on what you offer professionally: your fitness instruction and advice. If a client says your guidance caused an injury, was negligent, or pushed them too far — even if the claim is only perceived — this coverage may respond to protect your business.

Negligence is when you fail to exercise the care that a reasonable trainer would in a similar situation. Some examples include having a client:

- Perform exercises that are inappropriate for their condition

- Incorrectly perform exercises

- Lift weights that are too heavy

- Use defective equipment

- Use poor exercise form

You assess strength, endurance, and limits in real time. Even experienced trainers can make a call that doesn’t go as planned. Professional liability insurance helps ensure one mistake doesn’t derail the business you’ve worked hard to build.

Examples of Personal Trainer Professional Liability Claims

Here are some examples of professional liability claims for personal trainers.

- You create a custom workout plan, but during an intense session, the client injures their back and misses work. They claim your guidance was improper and sue for negligence.

- A client attempts a heavy lift during training, tears a shoulder muscle, and alleges you pushed them beyond safe limits. They take legal action over the injury.

- During an online yoga class, a beginner attempts an inversion (despite your modification offering), falls, and develops ongoing neck pain. They claim your instructions were unclear and file a claim against you.

Real-World Claim Example

During a coaching session, a client was using an indoor stair machine as part of her program when she fell and injured her shoulder. She alleged she had been left unattended and that the trainer failed to properly supervise the exercise. The trainer’s liability policy responded to cover the costs to make things right with the client.

Claim Payout: $170,000

General vs Professional Liability: Side-by-Side Comparison

General liability is designed to cover general third-party claims, such as client injuries or property damage. Professional liability may protect against claims related to your training expertise.

Be sure your insurance company checks all of these boxes.

| Feature | General Liability | Professional Liability |

|---|---|---|

|

Client injuries unrelated to your instruction |

✅ Typically covered |

❌ Not covered |

|

Client or studio property damage unrelated to your instruction |

✅ Typically covered |

❌ Not covered |

|

Professional mistakes that cause client injury |

❌ Not covered |

✅ Typically covered |

|

Typical claim examples |

A client slips over a dumbbell and suffers an injury during a session |

A client claims your physical cues were incorrect, which led to a muscle sprain |

|

Who needs it |

All trainers (especially for contract work) |

All trainers (especially those working independently) |

Many gyms, studios, and fitness centers require trainers to carry liability insurance! Learn more about how insurance helps you check off conditions for employment: Personal Trainer Insurance Requirements by State.

Why Do I Need Both General and Professional Liability Insurance?

You need both general and professional liability insurance to protect your business from multiple angles. Your risks fall into two main categories: what can happen around your sessions (general) and what can happen because of your instruction (professional).

These two coverages work together, like a warm-up and a cool-down, to keep your training business safe when things go wrong. They offer peace of mind so you can focus on supporting clients on their health journeys.

General and professional liability insurance offer essential protection for personal trainers. That’s why Insurance Canopy bundles both coverages into one simple policy — less guesswork over coverage, more workout planning! Learn more: What Is Personal Trainer Liability Insurance?

You need both general and professional liability insurance to protect your business from multiple angles. Your risks fall into two main categories: what can happen around your sessions (general) and what can happen because of your instruction (professional).

These two coverages work together, like a warm-up and a cool-down, to keep your training business safe when things go wrong. They offer peace of mind so you can focus on supporting clients on their health journeys.

What Other Coverages Does General Liability Insurance for Personal Trainers Include?

General liability insurance from Insurance Canopy also includes:

- Personal and advertising injury coverage, for non-physical damages, like libel, slander, or advertising mistakes

- Products and completed operations coverage, for the products you use during sessions and your completed services (i.e., a completed training session)

- Damage to premises rented coverage, in case you or your clients accidentally damage your rented space, such as a fitness studio

- Medical expense limit, to pay for third-party medical expenses, whether or not you’re at fault

Protect Your Operations and Instruction in 10 Minutes

Insurance Canopy offers affordable, top-rated personal trainer coverage that combines general and professional liability, plus optional add-ons for your gear, cyber liability, and more.

Buy a policy online in 10 minutes or less and get instant proof of insurance right through your user dashboard. Our coverage makes it easy to protect your business and coach responsibly, knowing you have a financial safety net in place!

FAQs About General Liability vs Professional Liability for Personal Trainers

How Much Is Liability Insurance for Personal Trainers?

Insurance Canopy’s personal trainer insurance cost starts at $15/month or $159/year, with optional add-on coverages available. For less than the price of your protein powder a month, you get excellent-rated coverage that doesn’t break the bank.

What Should I Look for When Comparing Personal Trainer Insurance?

When shopping for personal trainer insurance, make sure your policy checks all of these boxes:

✔️My modalities are covered

✔️The pricing fits my budget

✔️Coverage limits are at least $2 million per occurrence and $3 million aggregate

✔️I can customize my base policy with endorsements like additional insureds or gear and equipment (inland marine) coverage

✔️Customer support is provided by U.S.-based, licensed agents

Insurance Canopy meets all the above criteria, so you can feel confident about your trainer coverage.

Does Professional Liability Cover Nutrition or Meal Plans?

Professional liability for personal trainers does not cover nutrition or meal plans. If you offer general nutrition or services, a diet and nutrition coverage endorsement may help cover this business service.

Learn more about personal training and nutrition liability: Video: Can Personal Trainers Give Nutrition Advice?

If I Have an LLC, Do I Still Need Trainer Liability Insurance?

Yes, even if you have an LLC, you still need trainer liability insurance. An LLC helps separate your personal assets from your business, but it doesn’t prevent you from being sued or help pay for legal defense, settlements, or judgments.

Liability insurance is what helps cover the costs of liability claims, so you don’t have to pay out of pocket if something goes wrong.

Does My Gym’s Insurance Cover Me?

Most independent personal trainers are not covered by their gym’s liability insurance. In fact, many facilities require proof of your active coverage before you can train there. Having your own policy protects your business wherever you coach and sets you apart as a prepared, professional trainer.

Chelsea Ramsey, ACE CPT | Copywriter

Ohio-based copywriter and licensed insurance agent Chelsea Ramsey leverages her experiences as an American Council on Exercise (ACE) certified personal trainer, a role-playing game writer, and a former auto claims adjuster. She holds a bachelor’s in English from Ohio State University and a TEFL certification from Oxford Seminars. Before working at Veracity, Chelsea wrote for Zulily and trained clients at her local community center. She now writes to assist fitness professionals and entertainers in finding their ideal insurance policies.

Ohio-based copywriter and licensed insurance agent Chelsea Ramsey leverages her experiences as an American Council on Exercise (ACE) certified personal trainer, a role-playing game writer, and a former auto claims adjuster. She holds a bachelor’s in English from Ohio State University and a TEFL certification from Oxford Seminars. Before working at Veracity, Chelsea wrote for Zulily and trained clients at her local community center. She now writes to assist fitness professionals and entertainers in finding their ideal insurance policies.